Page 10 - Ch15_Computation of GST

P. 10

(iv) Input services 2,25,000 One invoice dated 20th January of preceding financial year on

which GST payable was ₹ 50,000 was missing and has been

found in October

Compute the net GST payable in cash by M/s. Flow Pro for October assuming that all the inward

supplies are inter-State supplies, and all outward supplies are intra-State supplies. Assume the rates

of taxes to be as under:

Particulars Rate of tax

CGST 9%

SGST 9%

IGST 18%

Make suitable assumptions, wherever necessary. All the conditions necessary for availing the ITC have

been fulfilled. Opening balance of the input tax credit for the relevant period is Nil. The annual return

for the previous financial year was filed on 15th September of the current year. [CA Inter MTP Mar 23]

Answer :-

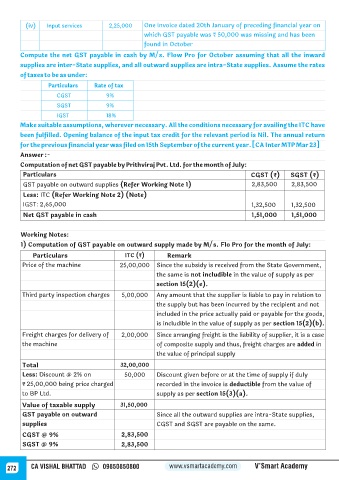

Computation of net GST payable by Prithviraj Pvt. Ltd. for the month of July:

Particulars CGST (₹) SGST (₹)

GST payable on outward supplies (Refer Working Note 1) 2,83,500 2,83,500

Less: ITC (Refer Working Note 2) (Note)

IGST: 2,65,000 1,32,500 1,32,500

Net GST payable in cash 1,51,000 1,51,000

Working Notes:

1) Computation of GST payable on outward supply made by M/s. Flo Pro for the month of July:

Particulars ITC (₹) Remark

Price of the machine 25,00,000 Since the subsidy is received from the State Government,

the same is not includible in the value of supply as per

section 15(2)(e).

Third party inspection charges 5,00,000 Any amount that the supplier is liable to pay in relation to

the supply but has been incurred by the recipient and not

included in the price actually paid or payable for the goods,

is includible in the value of supply as per section 15(2)(b).

Freight charges for delivery of 2,00,000 Since arranging freight is the liability of supplier, it is a case

the machine of composite supply and thus, freight charges are added in

the value of principal supply

Total 32,00,000

Less: Discount @ 2% on 50,000 Discount given before or at the time of supply if duly

₹ 25,00,000 being price charged recorded in the invoice is deductible from the value of

to BP Ltd. supply as per section 15(3)(a).

Value of taxable supply 31,50,000

GST payable on outward Since all the outward supplies are intra-State supplies,

supplies CGST and SGST are payable on the same.

CGST @ 9% 2,83,500

SGST @ 9% 2,83,500

272 CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy