Page 9 - Ch15_Computation of GST

P. 9

Notes:

1) Ü Since goods are agreed to be delivered at customer's doorsteps, supply of air- conditioners

along with transportation thereof is a composite supply which is treated as the supply of the

principal supply.

Ü Accordingly, rate of principal supply, i.e. air-conditioners will be charged.

2) Since parts/ spares and repair services are not naturally bundled, they are taxable separately at

the applicable rates.

3) Ü Since supplies are not naturally bundled and a single price is being charged, it is a mixed supply.

Ü It is treated as supply of that particular supply which attracts highest tax rate(i.e., stabilizers)

4) Ü IGST credit is first utilized for payment of IGST liability. Remaining IGST credit has been

utilised for payment of CGST and SGST in such proportion to keep the liability at its minimum.

Ü After exhausting IGST credit, CGST and SGST credits have been utilized. CGST credit is utilized for

payment of CGST and SGST credit is utilised for the payment of SGST.

Ü ITC of CGST cannot be utilized for payment of SGST and vice versa.

5) Ü Not exempt, since air travel embarking from Assam is not being undertaken in economy class.

Ü Further, ITC is available since service is used in the course/furtherance of business

6) ITC in respect of any invoice can be taken upto 30th November following the end of FY to which

such invoice relates or furnishing of the relevant annual return, whichever is earlier.

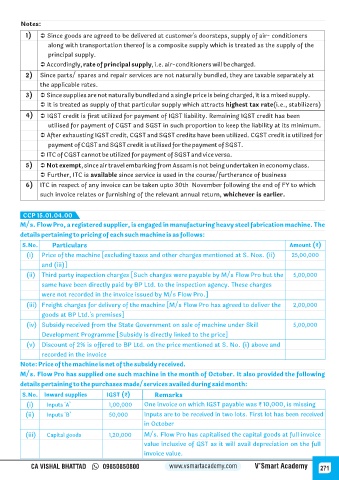

CCP 15.01.04.00

M/s. Flow Pro, a registered supplier, is engaged in manufacturing heavy steel fabrication machine. The

details pertaining to pricing of each such machine is as follows:

S.No. Particulars Amount (₹)

(i) Price of the machine [excluding taxes and other charges mentioned at S. Nos. (ii) 25,00,000

and (iii)]

(ii) Third party inspection charges [Such charges were payable by M/s Flow Pro but the 5,00,000

same have been directly paid by BP Ltd. to the inspection agency. These charges

were not recorded in the invoice issued by M/s Flow Pro.]

(iii) Freight charges for delivery of the machine [M/s Flow Pro has agreed to deliver the 2,00,000

goods at BP Ltd.'s premises]

(iv) Subsidy received from the State Government on sale of machine under Skill 5,00,000

Development Programme [Subsidy is directly linked to the price]

(v) Discount of 2% is offered to BP Ltd. on the price mentioned at S. No. (i) above and

recorded in the invoice

Note: Price of the machine is net of the subsidy received.

M/s. Flow Pro has supplied one such machine in the month of October. It also provided the following

details pertaining to the purchases made/services availed during said month:

S.No. Inward supplies IGST (₹) Remarks

(i) Inputs 'A’ 1,00,000 One invoice on which IGST payable was ₹ 10,000, is missing

(ii) Inputs 'B’ 50,000 Inputs are to be received in two lots. First lot has been received

in October

(iii) Capital goods 1,20,000 M/s. Flow Pro has capitalised the capital goods at full invoice

value inclusive of GST as it will avail depreciation on the full

invoice value.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 271