Page 27 - Ch8_ EXEMPTION

P. 27

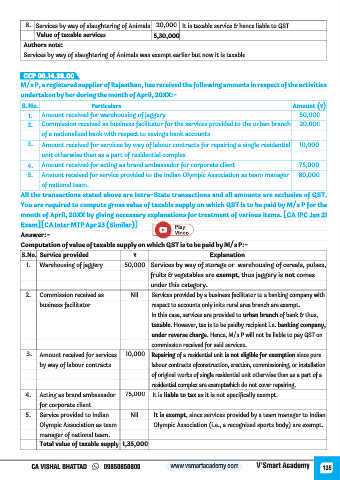

8. Services by way of slaughtering of Animals 20,000 It is taxable service & hence liable to GST

Value of taxable services 5,30,000

Authors note:

Services by way of slaughtering of Animals was exempt earlier but now it is taxable

CCP 08.14.28.00

M/s P, a registered supplier of Rajasthan, has received the following amounts in respect of the activities

undertaken by her during the month of April, 20XX:-

S.No. Particulars Amount (₹)

1. Amount received for warehousing of jaggery 50,000

2. Commission received as business facilitator for the services provided to the urban branch 20,000

of a nationalized bank with respect to savings bank accounts

3. Amount received for services by way of labour contracts for repairing a single residential 10,000

unit otherwise than as a part of residential complex

4. Amount received for acting as brand ambassador for corporate client 75,000

5. Amount received for service provided to the Indian Olympic Association as team manager 80,000

of national team.

All the transactions stated above are Intra-State transactions and all amounts are exclusive of GST.

You are required to compute gross value of taxable supply on which GST is to be paid by M/s P for the

month of April, 20XX by giving necessary explanations for treatment of various items. [CA IPC Jan 21

Exam] [CA Inter MTP Apr 23 (Similar)]

Answer:-

Computation of value of taxable supply on which GST is to be paid by M/s P:-

S.No. Service provided ₹ Explanation

1. Warehousing of jaggery 50,000 Services by way of storage or warehousing of cereals, pulses,

fruits & vegetables are exempt, thus jaggery is not comes

under this category.

2. Commission received as Nil Services provided by a business facilitator to a banking company with

business facilitator respect to accounts only inits rural area branch are exempt.

In this case, services are provided to urban branch of bank & thus,

taxable. However, tax is to be paidby recipient i.e. banking company,

under reverse charge. Hence, M/s P will not be liable to pay GST on

commission received for said services.

3. Amount received for services 10,000 Repairing of a residential unit is not eligible for exemption since pure

by way of labour contracts labour contracts ofconstruction, erection, commissioning, or installation

of original works of single residential unit otherwise than as a part of a

residential complex are exemptwhich do not cover repairing.

4. Acting as brand ambassador 75,000 It is liable to tax as it is not specifically exempt.

for corporate client

5. Service provided to Indian Nil It is exempt, since services provided by a team manager to Indian

Olympic Association as team Olympic Association (i.e., a recognized sports body) are exempt.

manager of national team.

Total value of taxable supply 1,35,000

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 135