Page 29 - Ch8_ EXEMPTION

P. 29

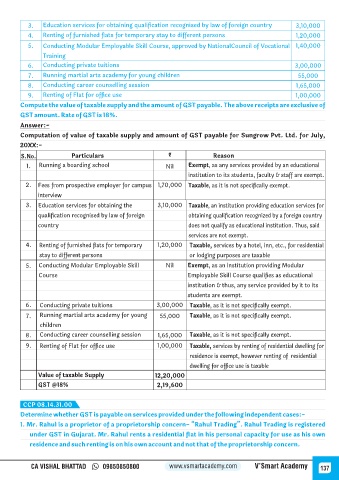

3. Education services for obtaining qualification recognised by law of foreign country 3,10,000

4. Renting of furnished flats for temporary stay to different persons 1,20,000

5. Conducting Modular Employable Skill Course, approved by NationalCouncil of Vocational 1,40,000

Training

6. Conducting private tuitions 3,00,000

7. Running martial arts academy for young children 55,000

8. Conducting career counselling session 1,65,000

9. Renting of Flat for office use 1,00,000

Compute the value of taxable supply and the amount of GST payable. The above receipts are exclusive of

GST amount. Rate of GST is 18%.

Answer:-

Computation of value of taxable supply and amount of GST payable for Sungrow Pvt. Ltd. for July,

20XX:-

S.No. Particulars ₹ Reason

1. Running a boarding school Nil Exempt, as any services provided by an educational

institution to its students, faculty & staff are exempt.

2. Fees from prospective employer for campus 1,70,000 Taxable, as it is not specifically exempt.

interview

3. Education services for obtaining the 3,10,000 Taxable, an institution providing education services for

qualification recognised by law of foreign obtaining qualification recognized by a foreign country

country does not qualify as educational institution. Thus, said

services are not exempt.

4. Renting of furnished flats for temporary 1,20,000 Taxable, services by a hotel, inn, etc., for residential

stay to different persons or lodging purposes are taxable

5. Conducting Modular Employable Skill Nil Exempt, as an institution providing Modular

Course Employable Skill Course qualifies as educational

institution & thus, any service provided by it to its

students are exempt.

6. Conducting private tuitions 3,00,000 Taxable, as it is not specifically exempt.

7. Running martial arts academy for young 55,000 Taxable, as it is not specifically exempt.

children

8. Conducting career counselling session 1,65,000 Taxable, as it is not specifically exempt.

9. Renting of Flat for office use 1,00,000 Taxable, services by renting of residential dwelling for

residence is exempt, however renting of residential

dwelling for office use is taxable

Value of taxable Supply 12,20,000

GST @18% 2,19,600

CCP 08.14.31.00

Determine whether GST is payable on services provided under the following independent cases:-

1. Mr. Rahul is a proprietor of a proprietorship concern- “Rahul Trading”. Rahul Trading is registered

under GST in Gujarat. Mr. Rahul rents a residential flat in his personal capacity for use as his own

residence and such renting is on his own account and not that of the proprietorship concern.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 137