Page 12 - CA Inter Audit PARAM

P. 12

CA Ravi Taori

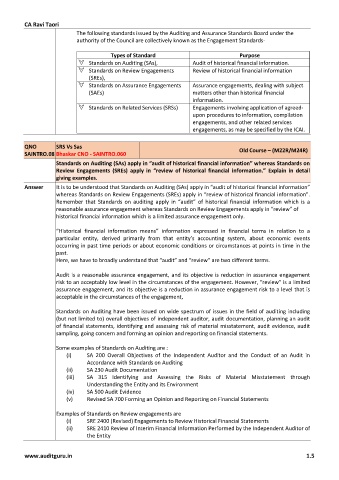

The following standards issued by the Auditing and Assurance Standards Board under the

authority of the Council are collectively known as the Engagement Standards-

Types of Standard Purpose

Standards on Auditing (SAs), Audit of historical financial information.

Standards on Review Engagements Review of historical financial information

(SREs),

Standards on Assurance Engagements Assurance engagements, dealing with subject

(SAEs) matters other than historical financial

information.

Standards on Related Services (SRSs) Engagements involving application of agreed-

upon procedures to information, compilation

engagements, and other related services

engagements, as may be specified by the ICAI.

QNO SRS Vs Sas Old Course – (M22R/M24R)

SAINTRO.08 Bhaskar CNO - SAINTRO.060

Standards on Auditing (SAs) apply in “audit of historical financial information” whereas Standards on

Review Engagements (SREs) apply in “review of historical financial information.” Explain in detail

giving examples.

Answer It is to be understood that Standards on Auditing (SAs) apply in “audit of historical financial information”

whereas Standards on Review Engagements (SREs) apply in “review of historical financial information”.

Remember that Standards on auditing apply in “audit” of historical financial information which is a

reasonable assurance engagement whereas Standards on Review Engagements apply in “review” of

historical financial information which is a limited assurance engagement only.

“Historical financial information means” information expressed in financial terms in relation to a

particular entity, derived primarily from that entity’s accounting system, about economic events

occurring in past time periods or about economic conditions or circumstances at points in time in the

past.

Here, we have to broadly understand that “audit” and “review” are two different terms.

Audit is a reasonable assurance engagement, and its objective is reduction in assurance engagement

risk to an acceptably low level in the circumstances of the engagement. However, “review” is a limited

assurance engagement, and its objective is a reduction in assurance engagement risk to a level that is

acceptable in the circumstances of the engagement,

Standards on Auditing have been issued on wide spectrum of issues in the field of auditing including

(but not limited to) overall objectives of independent auditor, audit documentation, planning an audit

of financial statements, identifying and assessing risk of material misstatement, audit evidence, audit

sampling, going concern and forming an opinion and reporting on financial statements.

Some examples of Standards on Auditing are :

(i) SA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in

Accordance with Standards on Auditing

(ii) SA 230 Audit Documentation

(iii) SA 315 Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and its Environment

(iv) SA 500 Audit Evidence

(v) Revised SA 700 Forming an Opinion and Reporting on Financial Statements

Examples of Standards on Review engagements are

(i) SRE 2400 (Revised) Engagements to Review Historical Financial Statements

(ii) SRE 2410 Review of Interim Financial Information Performed by the Independent Auditor of

the Entity

www.auditguru.in 1.5