Page 167 - CA Inter Audit PARAM

P. 167

CA Ravi Taori

QNO-- PPE - Elements of Cost New Course – (S24E)

AIFS.31.40 Bhaskar CNO – AIFS-P2.020

JB Limited has invested huge sums of money on establishment of new Property, Plant and Equipment during

the year under audit. They have incurred an amount of ₹ 5,70,000/- on dismantling of an old plant, which

had become obsolete, so that a new plant can be set up at the existing location. The Auditor is in the process

of verifying the cost incurred towards addition to Property, Plant and Equipment. What should be the

accounting treatment of the amount spent on dismantling of old plant in the financial statements? Which

elements of cost should be considered for valuing Property, Plant and Equipment?

Answer In the given situation, JB Limited has invested huge sums of money on establishment of new Property, Plant

and Equipment and incurred an amount of ₹ 5,70,000 on dismantling of old plant which had become

obsolete so that new plant can be set up at the existing location. An item of property, plant and equipment

that qualifies for recognition as an asset should be measured at its cost. The costs of dismantling, removing

the item and restoring the site on which it is located referred to as decommissioning will form part of the

new Property, Plant and Equipment.

Elements of Cost: The cost of an item of property, plant and equipment comprises:

(i) Its purchase price, including import duties and non-refundable purchase taxes, after deducting trade

discounts and rebates.

(ii) Any costs directly attributable to bringing the asset to the location and condition necessary for it to

be capable of operating in the manner intended by management.

(iii) The initial estimate of the costs of dismantling, removing the item and restoring the site on which it is

located, referred to as decommissioning, restoration and similar liabilities’, the obligation for which

an enterprise incurs either when the item is acquired or as a consequence of having used the item

during a particular period for purposes other than to produce inventories during that period.

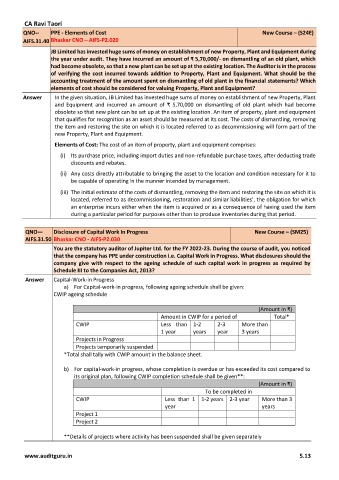

QNO— Disclosure of Capital Work In Progress New Course – (SM25)

AIFS.31.50 Bhaskar CNO - AIFS-P2.030

You are the statutory auditor of Jupiter Ltd. for the FY 2022-23. During the course of audit, you noticed

that the company has PPE under construction i.e. Capital Work in Progress. What disclosures should the

company give with respect to the ageing schedule of such capital work in progress as required by

Schedule III to the Companies Act, 2013?

Answer Capital-Work-in Progress

a) For Capital-work-in progress, following ageing schedule shall be given:

CWIP ageing schedule

(Amount in ₹)

Amount in CWIP for a period of Total*

CWIP Less than 1-2 2-3 More than

1 year years year 3 years

Projects in Progress

Projects temporarily suspended

*Total shall tally with CWIP amount in the balance sheet.

b) For capital-work-in progress, whose completion is overdue or has exceeded its cost compared to

its original plan, following CWIP completion schedule shall be given**:

(Amount in ₹)

To be completed in

CWIP Less than 1 1-2 years 2-3 year More than 3

year years

Project 1

Project 2

**Details of projects where activity has been suspended shall be given separately

www.auditguru.in 5.13