Page 321 - CA Inter Audit PARAM

P. 321

CA Ravi Taori

Answer Accounts regularized near the Balance Sheet Date: The asset classification of borrower accounts where a

solitary or a few credits are recorded before the balance sheet date should be handled with care and

without scope for subjectivity. Where the account indicates inherent weakness on the basis of the data

available, the account should be deemed as NPA.

The auditor should check for sample transactions immediately before the closing of the financial year and

immediately after the closing of the financial year to get a knowledge of the objective behind the

transactions if they have any relation to each other in the borrower accounts or if any/some transactions

are being reversed during the first few days after closing which might show an arrangement to prevent the

Borrower account(s) from slipping into the NPA category.

In the given case of Sidharth Industries, a payment of ₹ 10,00,000 was made on March 29, 2024 reducing

the outstanding loan balance to ₹ 40,00,000. and subsequently reversed by ₹ 8,00,000 on April 4, 2024.

Thus, Mahavir and Associates should carefully assess the classification of Sidharth Industries’ Account, and

determine if the payment and reversal transactions indicate an attempt to prevent the account from

slipping into the NPA category. If yes, the account should be classified as an NPA in compliance with

regulatory guidelines.

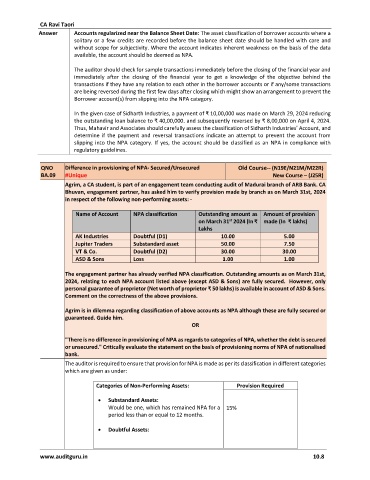

QNO Difference in provisioning of NPA- Secured/Unsecured Old Course-- (N19E/N21M/M22R)

BA.09 #Unique New Course – (J25R)

Agrim, a CA student, is part of an engagement team conducting audit of Madurai branch of ARB Bank. CA

Bhuvan, engagement partner, has asked him to verify provision made by branch as on March 31st, 2024

in respect of the following non-performing assets: -

Name of Account NPA classification Outstanding amount as Amount of provision

on March 31 2024 (In ₹ made (In ₹ lakhs)

st

Lakhs

AK Industries Doubtful (D1) 10.00 5.00

Jupiter Traders Substandard asset 50.00 7.50

VT & Co. Doubtful (D2) 30.00 30.00

ASD & Sons Loss 1.00 1.00

The engagement partner has already verified NPA classification. Outstanding amounts as on March 31st,

2024, relating to each NPA account listed above (except ASD & Sons) are fully secured. However, only

personal guarantee of proprietor (Net worth of proprietor ₹ 50 lakhs) is available in account of ASD & Sons.

Comment on the correctness of the above provisions.

Agrim is in dilemma regarding classification of above accounts as NPA although these are fully secured or

guaranteed. Guide him.

OR

"There is no difference in provisioning of NPA as regards to categories of NPA, whether the debt is secured

or unsecured." Critically evaluate the statement on the basis of provisioning norms of NPA of nationalised

bank.

The auditor is required to ensure that provision for NPA is made as per its classification in different categories

which are given as under:

Categories of Non-Performing Assets: Provision Required

Substandard Assets:

Would be one, which has remained NPA for a 15%

period less than or equal to 12 months.

Doubtful Assets:

www.auditguru.in 10.8