Page 319 - CA Inter Audit PARAM

P. 319

CA Ravi Taori

be considered as “significant”, requiring the asset to be classified as doubtful straightaway

and provided for adequately.

The realizable value of security as assessed by bank/approved valuers /RBI is less than 10%

of the outstanding in the borrower accounts, the existence of the security should be

ignored, and the asset should be classified as loss asset. In such cases the asset should either

be written off or fully provided for.

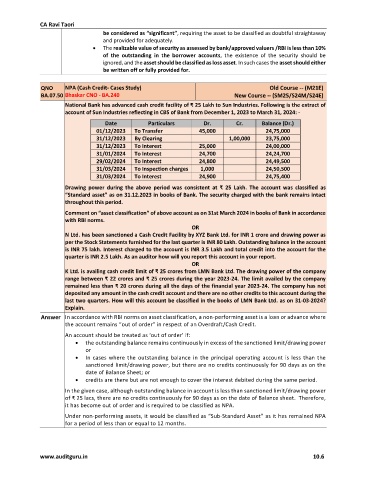

QNO NPA (Cash Credit- Cases Study) Old Course -- (M21E)

BA.07.50 Bhaskar CNO - BA.240 New Course -- (SM25/S24M/S24E)

National Bank has advanced cash credit facility of ₹ 25 Lakh to Sun Industries. Following is the extract of

account of Sun Industries reflecting in CBS of Bank from December 1, 2023 to March 31, 2024: -

Date Particulars Dr. Cr. Balance (Dr.)

01/12/2023 To Transfer 45,000 24,75,000

31/12/2023 By Clearing 1,00,000 23,75,000

31/12/2023 To Interest 25,000 24,00,000

31/01/2024 To Interest 24,700 24,24,700

29/02/2024 To Interest 24,800 24,49,500

31/03/2024 To Inspection charges 1,000 24,50,500

31/03/2024 To Interest 24,900 24,75,400

Drawing power during the above period was consistent at ₹ 25 Lakh. The account was classified as

“Standard asset” as on 31.12.2023 in books of Bank. The security charged with the bank remains intact

throughout this period.

Comment on “asset classification” of above account as on 31st March 2024 in books of Bank in accordance

with RBI norms.

OR

N Ltd. has been sanctioned a Cash Credit Facility by XYZ Bank Ltd. for INR 1 crore and drawing power as

per the Stock Statements furnished for the last quarter is INR 80 Lakh. Outstanding balance in the account

is INR 75 lakh. Interest charged to the account is INR 3.5 Lakh and total credit into the account for the

quarter is INR 2.5 Lakh. As an auditor how will you report this account in your report.

OR

K Ltd. is availing cash credit limit of ₹ 25 crores from LMN Bank Ltd. The drawing power of the company

range between ₹ 22 crores and ₹ 25 crores during the year 2023-24. The limit availed by the company

remained less than ₹ 20 crores during all the days of the financial year 2023-24. The company has not

deposited any amount in the cash credit account and there are no other credits to this account during the

last two quarters. How will this account be classified in the books of LMN Bank Ltd. as on 31-03-2024?

Explain.

Answer In accordance with RBI norms on asset classification, a non-performing asset is a loan or advance where

the account remains “out of order” in respect of an Overdraft/Cash Credit.

An account should be treated as ‘out of order’ if:

the outstanding balance remains continuously in excess of the sanctioned limit/drawing power

or

In cases where the outstanding balance in the principal operating account is less than the

sanctioned limit/drawing power, but there are no credits continuously for 90 days as on the

date of Balance Sheet; or

credits are there but are not enough to cover the interest debited during the same period.

In the given case, although outstanding balance in account is less than sanctioned limit/drawing power

of ₹ 25 lacs, there are no credits continuously for 90 days as on the date of Balance sheet. Therefore,

it has become out of order and is required to be classified as NPA.

Under non-performing assets, it would be classified as “Sub-Standard Asset” as it has remained NPA

for a period of less than or equal to 12 months.

www.auditguru.in 10.6