Page 91 - CA Inter Bhaskar Vol 1

P. 91

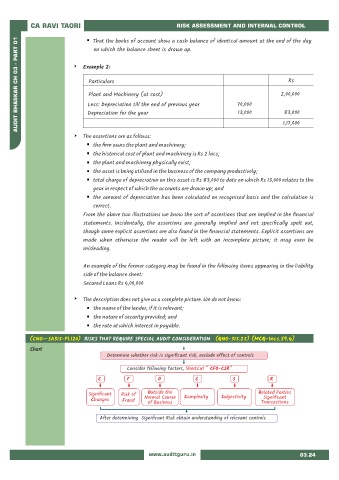

CA RAVI TAORI That the books of account show a cash balance of identical amount at the end of the day

RISK ASSESSMENT AND INTERNAL CONTROL

AUDIT BHASKAR CH 03 - PART 01 Example 2: 70,000 2,00,000

on which the balance sheet is drawn up.

Rs

Particulars

Plant and Machinery (at cost)

Less: Depreciation till the end of previous year

83,000

Depreciation for the year

The assertions are as follows: 13,000 1,17,000

the firm owns the plant and machinery;

the historical cost of plant and machinery is Rs 2 lacs;

the plant and machinery physically exist;

the asset is being utilised in the business of the company productively;

total charge of depreciation on this asset is Rs 83,000 to date on which Rs 13,000 relates to the

year in respect of which the accounts are drawn up; and

the amount of depreciation has been calculated on recognised basis and the calculation is

correct.

From the above two illustrations we know the sort of assertions that are implied in the financial

statements. Incidentally, the assertions are generally implied and not specifically spelt out,

though some explicit assertions are also found in the financial statements. Explicit assertions are

made when otherwise the reader will be left with an incomplete picture; it may even be

misleading.

An example of the former category may be found in the following items appearing in the liability

side of the balance sheet:

Secured Loans Rs 4,00,000

The description does not give us a complete picture. We do not know:

the name of the lender, if it is relevant;

the nature of security provided; and

the rate at which interest in payable.

(CNO—SA315-P1.120) RISKS THAT REQUIRE SPECIAL AUDIT CONSIDERATION (QNO-315.25) (MCQ-Incs.59.4)

Chart

Determine whether risk is significant risk, exclude effect of controls

Consider following factors, ShortCut “ CFO-CSR”

C F O C S R

Significant Risk of Outside the Complexity Subjectivity Related Parties

Changes Fraud Normal Course Significant

of Business Transactions

After determining Significant Risk obtain understanding of relevant controls

www.auditguru.in 03.24