Page 88 - CA Inter Bhaskar Vol 1

P. 88

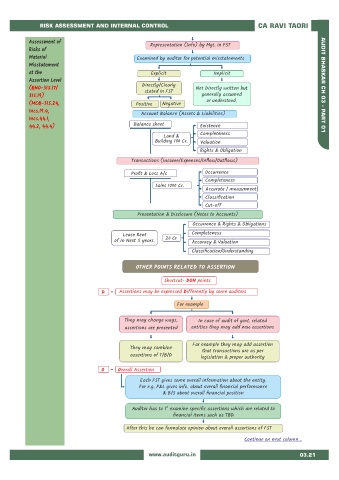

RISK ASSESSMENT AND INTERNAL CONTROL CA RAVI TAORI

Assessment of

Representation (Info) by Mgt. in FST

Risks of

Material Examined by auditor for potential misstatements

Misstatement

at the Explicit Implicit

Assertion Level

Directly/Clearly AUDIT BHASKAR CH 03 - PART 01

(QNO-315.17/ Not Directly written but

stated in FST

315.19) generally assumed

or understood.

(MCQ-315.24, Positive Negative

Incs.19.4,

Account Balance (Assets & Liabilities)

Incs.44.1,

Balance sheet

44.2, 44.4) Existence

Completeness

Land &

Building 100 Cr. Valuation

Rights & Obligation

Transactions (Income/Expenses/Inflow/Outflows)

Profit & Loss A/c Occurrence

Completeness

Sales 1000 Cr.

Accurate / measurment

Classification

Cut-off

Presentation & Disclosure (Notes to Accounts)

Occurrence & Rights & Obligations

Lease Rent Completeness

of In Next 5 years. 20 Cr Accuracy & Valuation

Classification/Understanding

OTHER POINTS RELATED TO ASSERTION

Shortcut- DON points

D Assertions may be expressed Differently by some auditors

For example

They may change ways, In case of audit of govt. related

assertions are presented entities they may add new assertions

Far example they may add assertion

They may combine

that transactions are as per

assertions of T/B/D

legislation & proper authority

O Overall Assertion

Each FST gives some overall information about the entity.

For e.g. P&L gives info. about overall financial performance

& B/S about overall financial position

st

Auditor has to 1 examine specific assertions which are related to

financial items such as TBD

After this he can formulate opinion about overall assertions of FST

Continue on next column...

www.auditguru.in 03.21