Page 4 - Chapter 1

P. 4

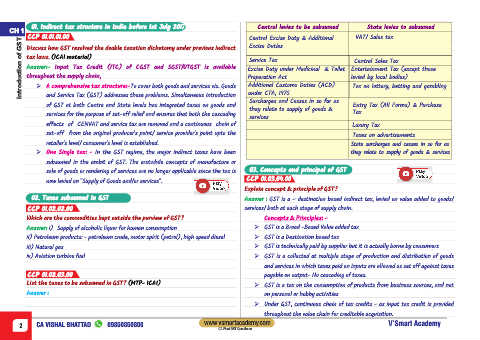

01. Indirect tax structure in India before 1st July 2017 Central levies to be subsumed State levies to subsumed

CH 1 Discuss how GST resolved the double taxation dichotomy under previous indirect Central Excise Duty & Additional VAT/ Sales tax

CCP 01.01.01.00

Introduction of GST tax laws. (ICAI material) Excise Duty under Medicinal & Toilet Entertainment Tax (except those

Excise Duties

Service Tax

Central Sales Tax

Answer:- Input Tax Credit (ITC) of CGST and SGST/UTGST is available

throughout the supply chain,

levied by local bodies)

Preparation Act

Additional Customs Duties (ACD)

To cover both goods and services viz. Goods

Ø A comprehensive tax structure:-

under CTA, 1975

and Service Tax (GST) addresses these problems. Simultaneous introduction

Surcharges and Cesses in so far as Tax on lottery, betting and gambling

of GST at both Centre and State levels has integrated taxes on goods and Entry Tax (All Forms) & Purchase

they relate to supply of goods &

services for the purpose of set-off relief and ensures that both the cascading Tax

services

effects of CENVAT and service tax are removed and a continuous chain of Luxury Tax

set-off from the original producer's point/ service provider's point upto the Taxes on advertisements

retailer's level/ consumer's level is established. State surcharges and cesses in so far as

Ø One Single tax: - In the GST regime, the major indirect taxes have been they relate to supply of goods & services

subsumed in the ambit of GST. The erstwhile concepts of manufacture or

sale of goods or rendering of services are no longer applicable since the tax is 03. Concepts and principal of GST

now levied on "Supply of Goods and/or services". CCP 01.03.04.00

Explain concept & principle of GST?

02. Taxes subsumed in GST Answer : GST is a – destination based indirect tax, levied on value added to goods/

CCP 01.02.02.00 services/ both at each stage of supply chain.

Which are the commodities kept outside the purview of GST? Concepts & Principles: -

Answer: i) Supply of alcoholic liquor for human consumption Ø GST is a Broad -Based Value added tax

ii) Petroleum products: - petroleum crude, motor spirit (petrol), high speed diesel Ø GST is a Destination based tax

iii) Natural gas Ø GST is technically paid by supplier but it is actually borne by consumers

iv) Aviation turbine fuel Ø GST is a collected at multiple stage of production and distribution of goods

and services in which taxes paid on inputs are allowed as set off against taxes

CCP 01.02.03.00 payable on output- No cascading of taxes.

List the taxes to be subsumed in GST? (MTP- ICAI) Ø GST is a tax on the consumption of products from business sources, and not

Answer : on personal or hobby activities

Ø Under GST, continuous chain of tax credits - as input tax credit is provided

throughout the value chain for creditable acquisition.

www.vsmartacademy.com

2 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner