Page 33 - Chapter 2.cdr

P. 33

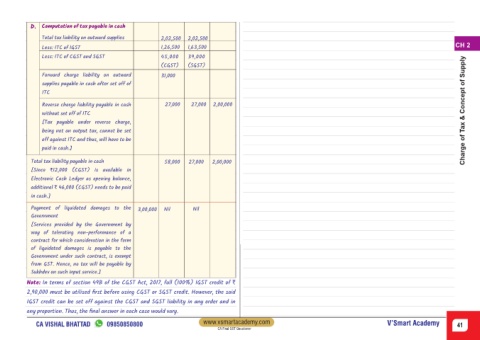

D. Computation of tax payable in cash

Total tax liability on outward supplies 2,02,500 2,02,500

CH 2

Less: ITC of IGST 1,26,500 1,63,500

Less: ITC of CGST and SGST 45,000 39,000

(CGST) (SGST)

Forward charge liability on outward 31,000

supplies payable in cash after set off of

ITC

Reverse charge liability payable in cash 27,000 27,000 2,00,000

without set off of ITC Charge of Tax & Concept of Supply

[Tax payable under reverse charge,

being not an output tax, cannot be set

off against ITC and thus, will have to be

paid in cash.]

Total tax liability payable in cash 58,000 27,000 2,00,000

[Since `12,000 (CGST) is available in

Electronic Cash Ledger as opening balance,

additional ` 46,000 (CGST) needs to be paid

in cash.]

Payment of liquidated damages to the 3,00,000 Nil Nil

Government

[Services provided by the Government by

way of tolerating non-performance of a

contract for which consideration in the form

of liquidated damages is payable to the

Government under such contract, is exempt

from GST. Hence, no tax will be payable by

Sukhdev on such input service.]

Note: In terms of section 49B of the CGST Act, 2017, full (100%) IGST credit of `

2,90,000 must be utilised first before using CGST or SGST credit. However, the said

IGST credit can be set off against the CGST and SGST liability in any order and in

any proportion. Thus, the final answer in each case would vary.

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 41

CA Final GST Questioner