Page 31 - Chapter 2.cdr

P. 31

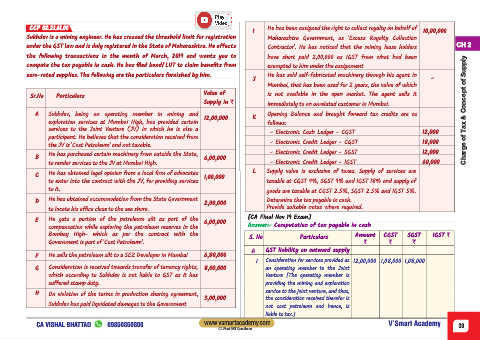

CCP 02.21.61.00 He has been assigned the right to collect royalty on behalf of

I 10,00,000

Sukhdev is a mining engineer. He has crossed the threshold limit for registration Maharashtra Government, as 'Excess Royalty Collection

under the GST law and is duly registered in the State of Maharashtra. He effects Contractor'. He has noticed that the mining lease holders CH 2

the following transactions in the month of March, 2019 and wants you to have short paid 2,00,000 as IGST from what had been

compute the tax payable in cash. He has filed bond/ LUT to claim benefits from exempted to him under the assignment

zero-rated supplies. The following are the particulars furnished by him. He has sold self-fabricated machinery through his agent in

J -

Mumbai, that has been used for 2 years, the value of which

Value of

Sr.No Particulars is not available in the open market. The agent sells it

Supply in ` immediately to an unrelated customer in Mumbai.

A Sukhdev, being an operating member in mining and Opening Balance and brought forward tax credits are as Charge of Tax & Concept of Supply

12,00,000 K

exploration services at Mumbai High, has provided certain follows:

services to the Joint Venture (JV) in which he is also a

- Electronic Cash Ledger - CGST 12,000

participant. He believes that the consideration received from

- Electronic Credit Ledger - CGST 18,000

the JV is 'Cost Petroleum' and not taxable.

He has purchased certain machinery from outside the State, - Electronic Credit Ledger - SGST 12,000

B 6,00,000

to render services to the JV at Mumbai High. - Electronic Credit Ledger - IGST 60,000

C He has obtained legal opinion from a local firm of advocates 1,00,000 L Supply value is exclusive of taxes. Supply of services are

to enter into the contract with the JV, for providing services taxable at CGST 9%, SGST 9% and IGST 18% and supply of

to it.

goods are taxable at CGST 2.5%, SGST 2.5% and IGST 5%.

D He has obtained accommodation from the State Government Determine the tax payable in cash.

2,00,000

to locate his office close to the sea shore. Provide suitable notes where required.

E He gets a portion of the petroleum silt as part of the [CA Final Nov 19 Exam]

6,00,000

compensation while exploring the petroleum reserves in the Answer:- Computation of tax payable in cash

Bombay High- which as per the contract with the Amount CGST SGST IGST `

S. No Particulars

Government is part of 'Cost Petroleum'. ` ` `

A GST liability on outward supply

F He sells the petroleum silt to a SEZ Developer in Mumbai 6,80,000

I Consideration for services provided as 12,00,000 1,08,000 1,08,000

G Consideration is received towards transfer of tenancy rights, 8,00,000 an operating member to the Joint

which according to Sukhdev is not liable to GST as it has Venture [The operating member is

suffered stamp duty. providing the mining and exploration

service to the joint venture, and thus,

H On violation of the terms in production sharing agreement,

3,00,000 the consideration received therefor is

Sukhdev has paid liquidated damages to the Government

not cost petroleum and hence, is

liable to tax.]

CA VISHAL BHATTAD 09850850800 www.vsmartacademy.com V’Smart Academy 39

CA Final GST Questioner