Page 30 - Chapter 2.cdr

P. 30

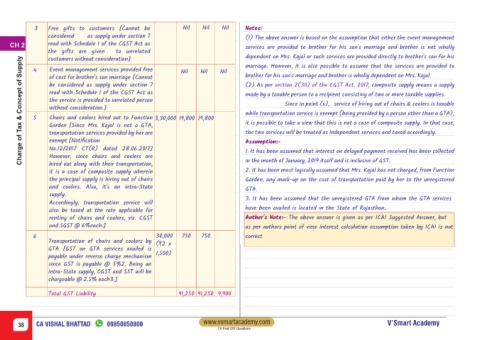

3 Free gifts to customers [Cannot be Nil Nil Nil Notes:

considered as supply under section 7 (1) The above answer is based on the assumption that either the event management

CH 2 read with Schedule I of the CGST Act as services are provided to brother for his son's marriage and brother is not wholly

the gifts are given to unrelated

dependent on Mrs. Kajal or such services are provided directly to brother's son for his

Charge of Tax & Concept of Supply

customers without consideration]

marriage. However, it is also possible to assume that the services are provided to

4 Event management services provided free Nil Nil Nil

of cost for brother's son marriage [Cannot brother for his son's marriage and brother is wholly dependent on Mrs. Kajal.

be considered as supply under section 7 (2) As per section 2(30) of the CGST Act, 2017 , composite supply means a supply

read with Schedule I of the CGST Act as made by a taxable person to a recipient consisting of two or more taxable supplies.

the service is provided to unrelated person

Since in point (v), service of hiring out of chairs & coolers is taxable

without consideration.]

while transportation service is exempt (being provided by a person other than a GTA),

5 Chairs and coolers hired out to Function 3,30,000 19,800 19,800

it is possible to take a view that this is not a case of composite supply. In that case,

Garden [Since Mrs. Kajal is not a GTA,

transportation services provided by her are the two services will be treated as independent services and taxed accordingly.

exempt [Notification Assumption:-

No.12/2017 CT(R) dated 28.06.2017]

1. It has been assumed that interest on delayed payment received has been collected

However, since chairs and coolers are

in the month of January, 2019 itself and is inclusive of GST.

hired out along with their transportation,

it is a case of composite supply wherein 2. It has been most logically assumed that Mrs. Kajal has not charged, from Function

the principal supply is hiring out of chairs Garden, any mark-up on the cost of transportation paid by her to the unregistered

and coolers. Also, it's an intra-State

GTA.

supply.

3. It has been assumed that the unregistered GTA from whom the GTA services

Accordingly, transportation service will

have been availed is located in the State of Rajasthan.

also be taxed at the rate applicable for

renting of chairs and coolers, viz. CGST Author's Note:- The above answer is given as per ICAI Suggested Answer, but

and SGST @ 6%each.] as per authors point of view interest calculation assumption taken by ICAI is not

6 30,000 750 750 correct

Transportation of chairs and coolers by

(`2 x

GTA [GST on GTA services availed is

1,500)

payable under reverse charge mechanism

since GST is payable @ 5%2. Being an

intra-State supply, CGST and SST will be

chargeable @ 2.5% each3.]

Total GST Liability 91,250 91,250 9,900

www.vsmartacademy.com

38 CA VISHAL BHATTAD 09850850800 V’Smart Academy

CA Final GST Questioner