Page 12 - 11. COMPILER QB - INDAS 105

P. 12

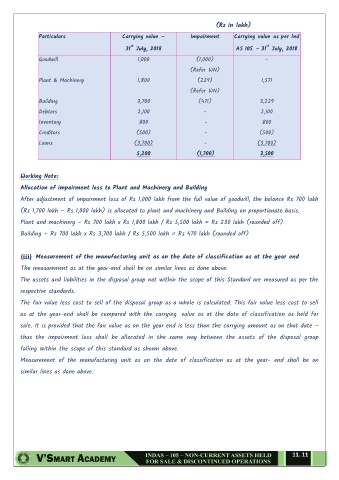

(Rs in lakh)

Particulars Carrying value – Impairment Carrying value as per Ind

st st

31 July, 2018 AS 105 – 31 July, 2018

Goodwill 1,000 (1,000) -

(Refer WN)

Plant & Machinery 1,800 (229) 1,571

(Refer WN)

Building 3,700 (471) 3,229

Debtors 2,100 - 2,100

Inventory 800 - 800

Creditors (500) - (500)

Loans (3,700) - (3,700)

5,200 (1,700) 3,500

Working Note:

Allocation of impairment loss to Plant and Machinery and Building

After adjustment of impairment loss of Rs 1,000 lakh from the full value of goodwill, the balance Rs 700 lakh

(Rs 1,700 lakh – Rs 1,000 lakh) is allocated to plant and machinery and Building on proportionate basis.

Plant and machinery – Rs 700 lakh x Rs 1,800 lakh / Rs 5,500 lakh = Rs 230 lakh (rounded off)

Building – Rs 700 lakh x Rs 3,700 lakh / Rs 5,500 lakh = Rs 470 lakh (rounded off)

(iii) Measurement of the manufacturing unit as on the date of classification as at the year end

The measurement as at the year-end shall be on similar lines as done above.

The assets and liabilities in the disposal group not within the scope of this Standard are measured as per the

respective standards.

The fair value less cost to sell of the disposal group as a whole is calculated. This fair value less cost to sell

as at the year-end shall be compared with the carrying value as at the date of classification as held for

sale. It is provided that the fair value as on the year end is less than the carrying amount as on that date –

thus the impairment loss shall be allocated in the same way between the assets of the disposal group

falling within the scope of this standard as shown above.

Measurement of the manufacturing unit as on the date of classification as at the year- end shall be on

similar lines as done above.

11. 11