Page 9 - 11. COMPILER QB - INDAS 105

P. 9

Solution

As per Ind AS 105 ‘Non-current Assets Held for Sale and Discontinued Operations’, an entity shall classify a

non-current asset as held for sale if its carrying amount will be recovered principally through a sale

transaction rather than through continuing use.

For asset to be classified as held for sale, it must be available for immediate sale in its present condition

subject only to terms that are usual and customary for sales of such assets and its sale must be highly

probable. In such a situation, an asset cannot be classified as a non-current asset held for sale, if the entity

intends to sell it in a distant future.

For the sale to be highly probable, the appropriate level of management must be committed to a plan to sell

the asset, and an active programme to locate a buyer and complete the plan must have been initiated.

Further, the asset must be actively marketed for sale at a price that is reasonable in relation to its current

fair value. In addition, the sale should be expected to qualify for recognition as a completed sale within one

year from the date of classification and actions required to complete the plan should indicate that it is

unlikely that significant changes to the plan will be made or that the plan will be withdrawn.

Further Ind AS 105 also states that an entity shall not classify as held for sale a non-current asset that is to

be abandoned. This is because its carrying amount will be recovered principally through continuing use.

An entity shall not account for a non-current asset that has been temporarily taken out of use as if it had

been abandoned.

In addition to Ind AS 105, Ind AS 16 states that depreciation does not cease when the asset becomes idle or

is retired from active use unless the asset is fully depreciated.

The Accountant of PB Ltd. has treated the plant as held for sale and measured it at the fair value less cost

to sell. Also, the depreciation has not been charged thereon since the date of classification as held for sale

which is not correct and not in accordance with Ind AS 105 and Ind AS 16.

Accordingly, the manufacturing plant should neither be treated as abandoned asset nor as held for sale

because its carrying amount will be principally recovered through continuous use. PB Ltd. shall not stop

charging depreciation or treat the plant as held for sale because its carrying amount will be recovered

principally through continuing use to the end of their economic life.

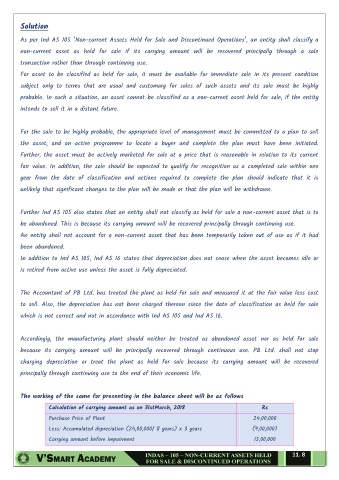

The working of the same for presenting in the balance sheet will be as follows

Calculation of carrying amount as on 31stMarch, 2018 Rs

Purchase Price of Plant 24,00,000

Less: Accumulated depreciation (24,00,000/ 8 years) x 3 years (9,00,000)

Carrying amount before impairment 15,00,000

11. 8