Page 10 - 11. COMPILER QB - INDAS 105

P. 10

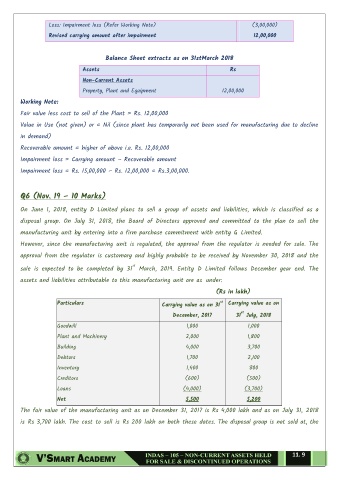

Less: Impairment loss (Refer Working Note) (3,00,000)

Revised carrying amount after impairment 12,00,000

Balance Sheet extracts as on 31stMarch 2018

Assets Rs

Non-Current Assets

Property, Plant and Equipment 12,00,000

Working Note:

Fair value less cost to sell of the Plant = Rs. 12,00,000

Value in Use (not given) or = Nil (since plant has temporarily not been used for manufacturing due to decline

in demand)

Recoverable amount = higher of above i.e. Rs. 12,00,000

Impairment loss = Carrying amount – Recoverable amount

Impairment loss = Rs. 15,00,000 – Rs. 12,00,000 = Rs.3,00,000.

Q6 (Nov. 19 – 10 Marks)

On June 1, 2018, entity D Limited plans to sell a group of assets and liabilities, which is classified as a

disposal group. On July 31, 2018, the Board of Directors approved and committed to the plan to sell the

manufacturing unit by entering into a firm purchase commitment with entity G Limited.

However, since the manufacturing unit is regulated, the approval from the regulator is needed for sale. The

approval from the regulator is customary and highly probable to be received by November 30, 2018 and the

st

sale is expected to be completed by 31 March, 2019. Entity D Limited follows December year end. The

assets and liabilities attributable to this manufacturing unit are as under:

(Rs in lakh)

Particulars Carrying value as on 31 st Carrying value as on

st

December, 2017 31 July, 2018

Goodwill 1,000 1,000

Plant and Machinery 2,000 1,800

Building 4,000 3,700

Debtors 1,700 2,100

Inventory 1,400 800

Creditors (600) (500)

Loans (4,000) (3,700)

Net 5,500 5,200

The fair value of the manufacturing unit as on December 31, 2017 is Rs 4,000 lakh and as on July 31, 2018

is Rs 3,700 lakh. The cost to sell is Rs 200 lakh on both these dates. The disposal group is not sold at, the

11. 9