Page 10 - 12. COMPILER QB - INDAS 19

P. 10

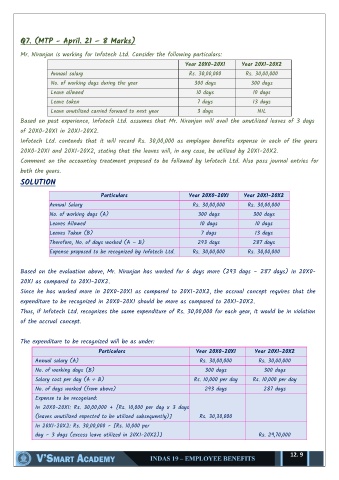

Q7. (MTP - April. 21 – 8 Marks)

Mr. Niranjan is working for Infotech Ltd. Consider the following particulars:

Year 20X0-20X1 Year 20X1-20X2

Annual salary Rs. 30,00,000 Rs. 30,00,000

No. of working days during the year 300 days 300 days

Leave allowed 10 days 10 days

Leave taken 7 days 13 days

Leave unutilized carried forward to next year 3 days NIL

Based on past experience, Infotech Ltd. assumes that Mr. Niranjan will avail the unutilized leaves of 3 days

of 20X0-20X1 in 20X1-20X2.

Infotech Ltd. contends that it will record Rs. 30,00,000 as employee benefits expense in each of the years

20X0-20X1 and 20X1-20X2, stating that the leaves will, in any case, be utilized by 20X1-20X2.

Comment on the accounting treatment proposed to be followed by Infotech Ltd. Also pass journal entries for

both the years.

SOLUTION

Particulars Year 20X0-20X1 Year 20X1-20X2

Annual Salary Rs. 30,00,000 Rs. 30,00,000

No. of working days (A) 300 days 300 days

Leaves Allowed 10 days 10 days

Leaves Taken (B) 7 days 13 days

Therefore, No. of days worked (A – B) 293 days 287 days

Expense proposed to be recognized by Infotech Ltd. Rs. 30,00,000 Rs. 30,00,000

Based on the evaluation above, Mr. Niranjan has worked for 6 days more (293 days – 287 days) in 20X0-

20X1 as compared to 20X1-20X2.

Since he has worked more in 20X0-20X1 as compared to 20X1-20X2, the accrual concept requires that the

expenditure to be recognized in 20X0-20X1 should be more as compared to 20X1-20X2.

Thus, if Infotech Ltd. recognizes the same expenditure of Rs. 30,00,000 for each year, it would be in violation

of the accrual concept.

The expenditure to be recognized will be as under:

Particulars Year 20X0-20X1 Year 20X1-20X2

Annual salary (A) Rs. 30,00,000 Rs. 30,00,000

No. of working days (B) 300 days 300 days

Salary cost per day (A ÷ B) Rs. 10,000 per day Rs. 10,000 per day

No. of days worked (from above) 293 days 287 days

Expense to be recognised:

In 20X0-20X1: Rs. 30,00,000 + [Rs. 10,000 per day x 3 days

(leaves unutilized expected to be utilized subsequently)] Rs. 30,30,000

In 20X1-20X2: Rs. 30,00,000 – [Rs. 10,000 per

day – 3 days (excess leave utilized in 20X1-20X2)] Rs. 29,70,000

12. 9