Page 9 - 12. COMPILER QB - INDAS 19

P. 9

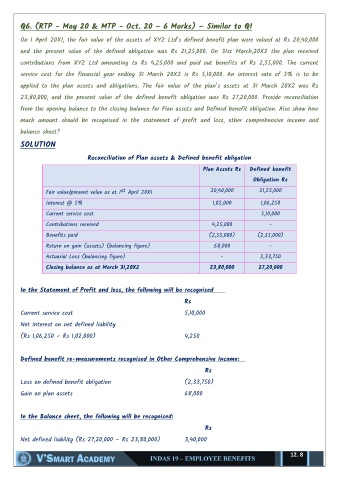

Q6. (RTP - May 20 & MTP - Oct. 20 – 6 Marks) – Similar to Q1

On 1 April 20X1, the fair value of the assets of XYZ Ltdʼs defined benefit plan were valued at Rs 20,40,000

and the present value of the defined obligation was Rs 21,25,000. On 31st March,20X2 the plan received

contributions from XYZ Ltd amounting to Rs 4,25,000 and paid out benefits of Rs 2,55,000. The current

service cost for the financial year ending 31 March 20X2 is Rs 5,10,000. An interest rate of 5% is to be

applied to the plan assets and obligations. The fair value of the planʼs assets at 31 March 20X2 was Rs

23,80,000, and the present value of the defined benefit obligation was Rs 27,20,000. Provide reconciliation

from the opening balance to the closing balance for Plan assets and Defined benefit obligation. Also show how

much amount should be recognised in the statement of profit and loss, other comprehensive income and

balance sheet?

SOLUTION

Reconciliation of Plan assets & Defined benefit obligation

Plan Assets Rs Defined benefit

Obligation Rs

Fair value/present value as at 1 st April 20X1 20,40,000 21,25,000

Interest @ 5% 1,02,000 1,06,250

Current service cost 5,10,000

Contributions received 4,25,000 -

Benefits paid (2,55,000) (2,55,000)

Return on gain (assets) (balancing figure) 68,000 -

Actuarial Loss (balancing figure) - 2,33,750

Closing balance as at March 31,20X2 23,80,000 27,20,000

In the Statement of Profit and loss, the following will be recognised

Rs

Current service cost 5,10,000

Net interest on net defined liability

(Rs 1,06,250 – Rs 1,02,000) 4,250

Defined benefit re-measurements recognised in Other Comprehensive Income:

Rs

Loss on defined benefit obligation (2,33,750)

Gain on plan assets 68,000

In the Balance sheet, the following will be recognised:

Rs

Net defined liability (Rs 27,20,000 – Rs 23,80,000) 3,40,000

12. 8