Page 3 - 12. COMPILER QB - INDAS 19

P. 3

st

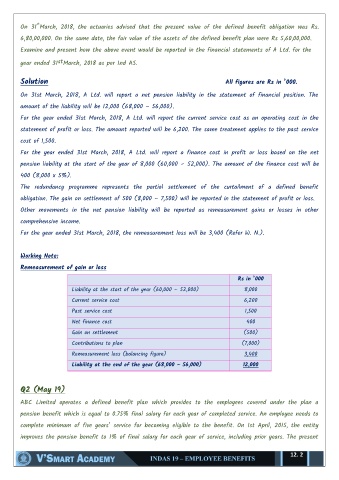

On 31 March, 2018, the actuaries advised that the present value of the defined benefit obligation was Rs.

6,80,00,000. On the same date, the fair value of the assets of the defined benefit plan were Rs 5,60,00,000.

Examine and present how the above event would be reported in the financial statements of A Ltd. for the

st

year ended 31 March, 2018 as per Ind AS.

Solution All figures are Rs in ’000.

On 31st March, 2018, A Ltd. will report a net pension liability in the statement of financial position. The

amount of the liability will be 12,000 (68,000 – 56,000).

For the year ended 31st March, 2018, A Ltd. will report the current service cost as an operating cost in the

statement of profit or loss. The amount reported will be 6,200. The same treatment applies to the past service

cost of 1,500.

For the year ended 31st March, 2018, A Ltd. will report a finance cost in profit or loss based on the net

pension liability at the start of the year of 8,000 (60,000 – 52,000). The amount of the finance cost will be

400 (8,000 x 5%).

The redundancy programme represents the partial settlement of the curtailment of a defined benefit

obligation. The gain on settlement of 500 (8,000 – 7,500) will be reported in the statement of profit or loss.

Other movements in the net pension liability will be reported as remeasurement gains or losses in other

comprehensive income.

For the year ended 31st March, 2018, the remeasurement loss will be 3,400 (Refer W. N.).

Working Note:

Remeasurement of gain or loss

Rs in ’000

Liability at the start of the year (60,000 – 52,000) 8,000

Current service cost 6,200

Past service cost 1,500

Net finance cost 400

Gain on settlement (500)

Contributions to plan (7,000)

Remeasurement loss (balancing figure) 3,400

Liability at the end of the year (68,000 – 56,000) 12,000

Q2 (May 19)

ABC Limited operates a defined benefit plan which provides to the employees covered under the plan a

pension benefit which is equal to 0.75% final salary for each year of completed service. An employee needs to

complete minimum of five years’ service for becoming eligible to the benefit. On 1st April, 2015, the entity

improves the pension benefit to 1% of final salary for each year of service, including prior years. The present

12. 2