Page 3 - 2. COMPILER QB - INDAS 12

P. 3

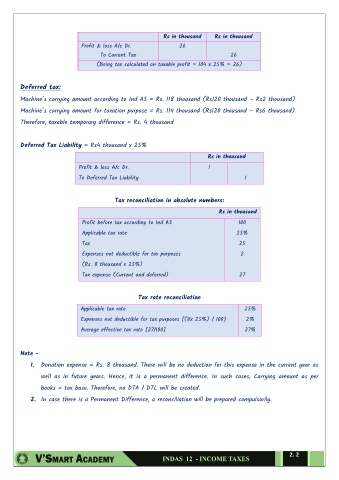

Rs in thousand Rs in thousand

Profit & loss A/c Dr. 26

To Current Tax 26

(Being tax calculated on taxable profit = 104 x 25% = 26)

Deferred tax:

Machine’s carrying amount according to Ind AS = Rs. 118 thousand (Rs120 thousand – Rs2 thousand)

Machine’s carrying amount for taxation purpose = Rs. 114 thousand (Rs120 thousand – Rs6 thousand)

Therefore, taxable temporary difference = Rs. 4 thousand

Deferred Tax Liability = Rs4 thousand x 25%

Rs in thousand

Profit & loss A/c Dr. 1

To Deferred Tax Liability 1

Tax reconciliation in absolute numbers:

Rs in thousand

Profit before tax according to Ind AS 100

Applicable tax rate 25%

Tax 25

Expenses not deductible for tax purposes 2

(Rs. 8 thousand x 25%)

Tax expense (Current and deferred) 27

Tax rate reconciliation

Applicable tax rate 25%

Expenses not deductible for tax purposes [(8x 25%) / 100] 2%

Average effective tax rate [27/100] 27%

Note -

1. Donation expense = Rs. 8 thousand. There will be no deduction for this expense in the current year as

well as in future years. Hence, it is a permanent difference. In such cases, Carrying amount as per

books = tax base. Therefore, no DTA / DTL will be created.

2. In case there is a Permanent Difference, a reconciliation will be prepared compulsorily.

2. 2