Page 8 - 2. COMPILER QB - INDAS 12

P. 8

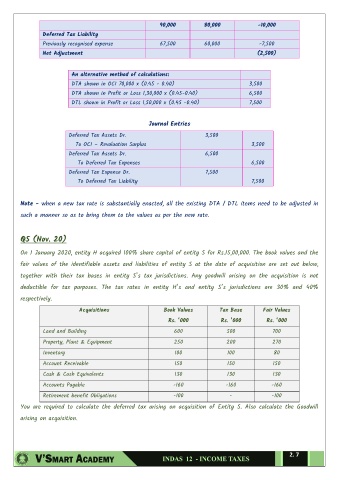

90,000 80,000 -10,000

Deferred Tax Liability

Previously recognised expense 67,500 60,000 -7,500

Net Adjustment (2,500)

An alternative method of calculations:

DTA shown in OCI 70,000 x (0.45 - 0.40) 3,500

DTA shown in Profit or Loss 1,30,000 x (0.45-0.40) 6,500

DTL shown in Profit or Loss 1,50,000 x (0.45 -0.40) 7,500

Journal Entries

Deferred Tax Assets Dr. 3,500

To OCI – Revaluation Surplus 3,500

Deferred Tax Assets Dr. 6,500

To Deferred Tax Expenses 6,500

Deferred Tax Expense Dr. 7,500

To Deferred Tax Liability 7,500

Note - when a new tax rate is substantially enacted, all the existing DTA / DTL items need to be adjusted in

such a manner so as to bring them to the values as per the new rate.

Q5 (Nov. 20)

On 1 January 2020, entity H acquired 100% share capital of entity S for Rs.15,00,000. The book values and the

fair values of the identifiable assets and liabilities of entity S at the date of acquisition are set out below,

together with their tax bases in entity S’s tax jurisdictions. Any goodwill arising on the acquisition is not

deductible for tax purposes. The tax rates in entity H’s and entity S’s jurisdictions are 30% and 40%

respectively.

Acquisitions Book Values Tax Base Fair Values

Rs. ‘000 Rs. ‘000 Rs. ‘000

Land and Building 600 500 700

Property, Plant & Equipment 250 200 270

Inventory 100 100 80

Account Receivable 150 150 150

Cash & Cash Equivalents 130 130 130

Accounts Payable -160 -160 -160

Retirement benefit Obligations -100 - -100

You are required to calculate the deferred tax arising on acquisition of Entity S. Also calculate the Goodwill

arising on acquisition.

2. 7