Page 17 - 6. COMPILER QB - INDAS 116

P. 17

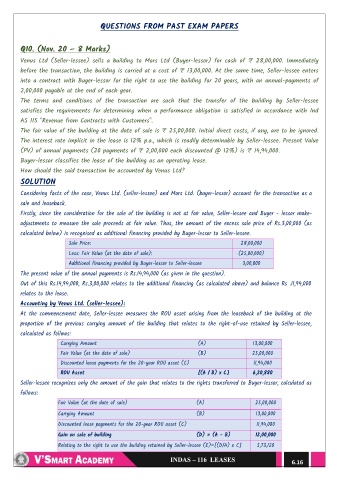

QUESTIONS FROM PAST EXAM PAPERS

Q10. (Nov. 20 – 8 Marks)

Venus Ltd (Seller-lessee) sells a building to Mars Ltd (Buyer-lessor) for cash of ₹ 28,00,000. Immediately

before the transaction, the building is carried at a cost of ₹ 13,00,000. At the same time, Seller-lessee enters

into a contract with Buyer-lessor for the right to use the building for 20 years, with an annual-payments of

2,00,000 payable at the end of each year.

The terms and conditions of the transaction are such that the transfer of the building by Seller-lessee

satisfies the requirements for determining when a performance obligation is satisfied in accordance with Ind

AS 115 "Revenue from Contracts with Customers".

The fair value of the building at the date of sale is ₹ 25,00,000. Initial direct costs, if any, are to be ignored.

The interest rate implicit in the lease is 12% p.a., which is readily determinable by Seller-lessee. Present Value

(PV) of annual payments (20 payments of ₹ 2,00,000 each discounted @ 12%) is ₹ 14,94,000.

Buyer-lessor classifies the lease of the building as an operating lease.

How should the said transaction be accounted by Venus Ltd?

SOLUTION

Considering facts of the case, Venus Ltd. (seller-lessee) and Mars Ltd. (buyer-lessor) account for the transaction as a

sale and leaseback.

Firstly, since the consideration for the sale of the building is not at fair value, Seller-lessee and Buyer - lessor make-

adjustments to measure the sale proceeds at fair value. Thus, the amount of the excess sale price of ₨.3,00,000 (as

calculated below) is recognised as additional financing provided by Buyer-lessor to Seller-lessee.

Sale Price: 28,00,000

Less: Fair Value (at the date of sale): (25,00,000)

Additional financing provided by Buyer-lessor to Seller-lessee 3,00,000

The present value of the annual payments is ₨.14,94,000 (as given in the question).

Out of this ₨.14,94,000, ₨.3,00,000 relates to the additional financing (as calculated above) and balance ₨ .11,94,000

relates to the lease.

Accounting by Venus Ltd. (seller-lessee):

At the commencement date, Seller-lessee measures the ROU asset arising from the leaseback of the building at the

proportion of the previous carrying amount of the building that relates to the right-of-use retained by Seller-lessee,

calculated as follows:

Carrying Amount (A) 13,00,000

Fair Value (at the date of sale) (B) 25,00,000

Discounted lease payments for the 20-year ROU asset (C) 11,94,000

ROU Asset [(A / B) x C] 6,20,880

Seller-lessee recognizes only the amount of the gain that relates to the rights transferred to Buyer-lessor, calculated as

follows:

Fair Value (at the date of sale) (A) 25,00,000

Carrying Amount (B) 13,00,000

Discounted lease payments for the 20-year ROU asset (C) 11,94,000

Gain on sale of building (D) = (A - B) 12,00,000

Relating to the right to use the building retained by Seller-lessee (E)=[(D/A) x C] 5,73,120

6.16