Page 15 - 6. COMPILER QB - INDAS 116

P. 15

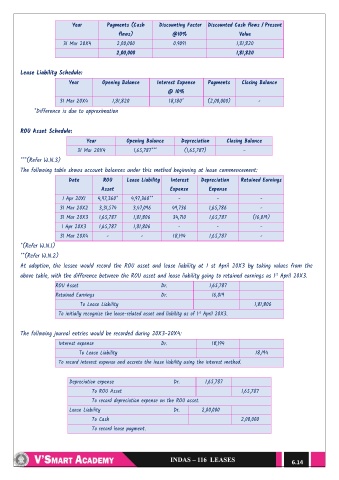

Year Payments (Cash Discounting Factor Discounted Cash flows / Present

flows) @10% Value

31 Mar 20X4 2,00,000 0.9091 1,81,820

2,00,000 1,81,820

Lease Liability Schedule:

Year Opening Balance Interest Expense Payments Closing Balance

@ 10%

31 Mar 20X4 1,81,820 18,180* (2,00,000) -

*Difference is due to approximation

ROU Asset Schedule:

Year Opening Balance Depreciation Closing Balance

31 Mar 20X4 1,65,787*** (1,65,787) -

***(Refer W.N.3)

The following table shows account balances under this method beginning at lease commencement:

Date ROU Lease Liability Interest Depreciation Retained Earnings

Asset Expense Expense

1 Apr 20X1 4,97,360* 4,97,360** - - -

31 Mar 20X2 3,31,574 3,47,096 49,736 1,65,786 -

31 Mar 20X3 1,65,787 1,81,806 34,710 1,65,787 (16,019)

1 Apr 20X3 1,65,787 1,81,806 - - -

31 Mar 20X4 - - 18,194 1,65,787 -

*(Refer W.N.1)

**(Refer W.N.2)

At adoption, the lessee would record the ROU asset and lease liability at 1 st April 20X3 by taking values from the

st

above table, with the difference between the ROU asset and lease liability going to retained earnings as 1 April 20X3.

ROU Asset Dr. 1,65,787

Retained Earnings Dr. 16,019

To Lease Liability 1,81,806

st

To initially recognise the lease-related asset and liability as of 1 April 20X3.

The following journal entries would be recorded during 20X3-20X4:

Interest expense Dr. 18,194

To Lease Liability 18,194

To record interest expense and accrete the lease liability using the interest method.

Depreciation expense Dr. 1,65,787

To ROU Asset 1,65,787

To record depreciation expense on the ROU asset.

Lease Liability Dr. 2,00,000

To Cash 2,00,000

To record lease payment.

6.14