Page 13 - 7. COMPILER QB - INDAS 2

P. 13

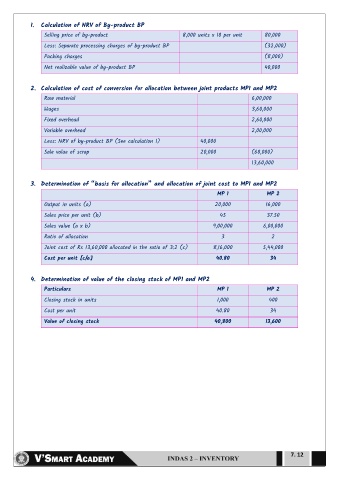

1. Calculation of NRV of By-product BP

Selling price of by-product 8,000 units x 10 per unit 80,000

Less: Separate processing charges of by-product BP (32,000)

Packing charges (8,000)

Net realizable value of by-product BP 40,000

2. Calculation of cost of conversion for allocation between joint products MP1 and MP2

Raw material 6,00,000

Wages 3,60,000

Fixed overhead 2,60,000

Variable overhead 2,00,000

Less: NRV of by-product BP (See calculation 1) 40,000

Sale value of scrap 20,000 (60,000)

13,60,000

3. Determination of “basis for allocation” and allocation of joint cost to MP1 and MP2

MP 1 MP 2

Output in units (a) 20,000 16,000

Sales price per unit (b) 45 37.50

Sales value (a x b) 9,00,000 6,00,000

Ratio of allocation 3 2

Joint cost of Rs 13,60,000 allocated in the ratio of 3:2 (c) 8,16,000 5,44,000

Cost per unit [c/a] 40.80 34

4. Determination of value of the closing stock of MP1 and MP2

Particulars MP 1 MP 2

Closing stock in units 1,000 400

Cost per unit 40.80 34

Value of closing stock 40,800 13,600

7. 12