Page 8 - 7. COMPILER QB - INDAS 2

P. 8

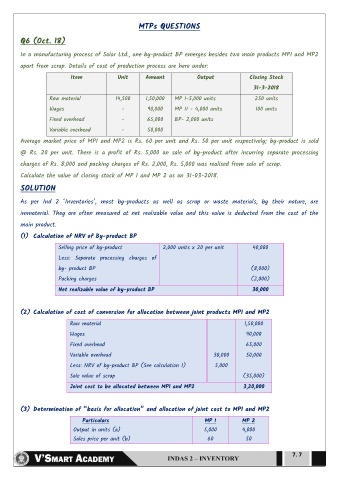

MTPs QUESTIONS

Q6 (Oct. 18)

In a manufacturing process of Solar Ltd., one by-product BP emerges besides two main products MP1 and MP2

apart from scrap. Details of cost of production process are here under:

Item Unit Amount Output Closing Stock

31-3-2018

Raw material 14,500 1,50,000 MP I-5,000 units 250 units

Wages - 90,000 MP II - 4,000 units 100 units

Fixed overhead - 65,000 BP- 2,000 units

Variable overhead - 50,000

Average market price of MP1 and MP2 is Rs. 60 per unit and Rs. 50 per unit respectively; by-product is sold

@ Rs. 20 per unit. There is a profit of Rs. 5,000 on sale of by-product after incurring separate processing

charges of Rs. 8,000 and packing charges of Rs. 2,000, Rs. 5,000 was realised from sale of scrap.

Calculate the value of closing stock of MP 1 and MP 2 as on 31-03-2018.

SOLUTION

As per Ind 2 ―Inventories‖, most by-products as well as scrap or waste materials, by their nature, are

immaterial. They are often measured at net realizable value and this value is deducted from the cost of the

main product.

(1) Calculation of NRV of By-product BP

Selling price of by-product 2,000 units x 20 per unit 40,000

Less: Separate processing charges of

by- product BP (8,000)

Packing charges (2,000)

Net realizable value of by-product BP 30,000

(2) Calculation of cost of conversion for allocation between joint products MP1 and MP2

Raw material 1,50,000

Wages 90,000

Fixed overhead 65,000

Variable overhead 30,000 50,000

Less: NRV of by-product BP (See calculation 1) 5,000

Sale value of scrap (35,000)

Joint cost to be allocated between MP1 and MP2 3,20,000

(3) Determination of “basis for allocation” and allocation of joint cost to MP1 and MP2

Particulars MP I MP 2

Output in units (a) 5,000 4,000

Sales price per unit (b) 60 50

7. 7