Page 38 - 16. COMPILER QB - INDAS 103

P. 38

its own equity. The balance of 2.5 will be recorded as employee expense in the books of D Ltd. over the

remaining life, which is 1 year in this scenario.

c. There is a difference between contingent consideration and deferred consideration. In the given case 35 is

the minimum payment to be paid after 2 years and accordingly will be considered as deferred

consideration. The other element is if a company meets a certain target then they will get 25% of that

or 35 whichever is higher. In the given case since the minimum what is expected to be paid the fair

value of the contingent consideration has been considered as zero. The impact of time value on deferred

consideration has been given @ 10%.

d. The additional consideration of Rs. 20 lakhs to be paid to the founder shareholder is contingent to

him/her continuing in employment and hence this will be considered as employee compensation and will

be recorded as post combination expenses in the income statement of D Ltd.

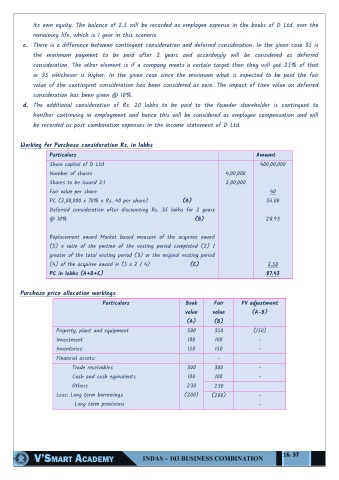

Working for Purchase consideration Rs. in lakhs

Particulars Amount

Share capital of D Ltd 400,00,000

Number of shares 4,00,000

Shares to be issued 2:1 2,00,000

Fair value per share 40

PC (2,00,000 x 70% x Rs. 40 per share) (A) 56.00

Deferred consideration after discounting Rs. 35 lakhs for 2 years

@ 10% (B) 28.93

Replacement award Market based measure of the acquiree award

(5) x ratio of the portion of the vesting period completed (2) /

greater of the total vesting period (3) or the original vesting period

(4) of the acquiree award ie (5 x 2 / 4) (C) 2.50

PC in lakhs (A+B+C) 87.43

Purchase price allocation workings

Particulars Book Fair FV adjustment

value value (A-B)

(A) (B)

Property, plant and equipment 500 350 (150)

Investment 100 100 -

Inventories 150 150 -

Financial assets: -

Trade receivables 300 300 -

Cash and cash equivalents 100 100 -

Others 230 230

Less: Long term borrowings (200) (200) -

Long term provisions -

16. 37