Page 31 - 20. COMPILER QB - INDAS 102

P. 31

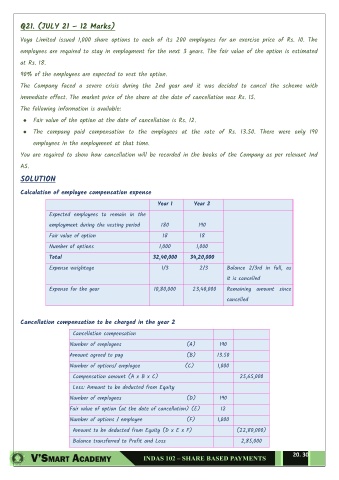

Q21. (JULY 21 – 12 Marks)

Voya Limited issued 1,000 share options to each of its 200 employees for an exercise price of Rs. 10. The

employees are required to stay in employment for the next 3 years. The fair value of the option is estimated

at Rs. 18.

90% of the employees are expected to vest the option.

The Company faced a severe crisis during the 2nd year and it was decided to cancel the scheme with

immediate effect. The market price of the share at the date of cancellation was Rs. 15.

The following information is available:

● Fair value of the option at the date of cancellation is Rs. 12.

● The company paid compensation to the employees at the rate of Rs. 13.50. There were only 190

employees in the employment at that time.

You are required to show how cancellation will be recorded in the books of the Company as per relevant Ind

AS.

SOLUTION

Calculation of employee compensation expense

Year 1 Year 2

Expected employees to remain in the

employment during the vesting period 180 190

Fair value of option 18 18

Number of options 1,000 1,000

Total 32,40,000 34,20,000

Expense weightage 1/3 2/3 Balance 2/3rd in full, as

it is cancelled

Expense for the year 10,80,000 23,40,000 Remaining amount since

cancelled

Cancellation compensation to be charged in the year 2

Cancellation compensation

Number of employees (A) 190

Amount agreed to pay (B) 13.50

Number of options/ employee (C) 1,000

Compensation amount (A x B x C) 25,65,000

Less: Amount to be deducted from Equity

Number of employees (D) 190

Fair value of option (at the date of cancellation) (E) 12

Number of options / employee (F) 1,000

Amount to be deducted from Equity (D x E x F) (22,80,000)

Balance transferred to Profit and Loss 2,85,000

20. 30