Page 29 - 20. COMPILER QB - INDAS 102

P. 29

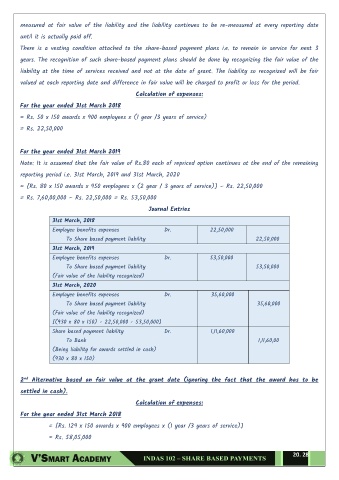

measured at fair value of the liability and the liability continues to be re-measured at every reporting date

until it is actually paid off.

There is a vesting condition attached to the share-based payment plans i.e. to remain in service for next 3

years. The recognition of such share-based payment plans should be done by recognizing the fair value of the

liability at the time of services received and not at the date of grant. The liability so recognized will be fair

valued at each reporting date and difference in fair value will be charged to profit or loss for the period.

Calculation of expenses:

For the year ended 31st March 2018

= Rs. 50 x 150 awards x 900 employees x (1 year /3 years of service)

= Rs. 22,50,000

For the year ended 31st March 2019

Note: It is assumed that the fair value of Rs.80 each of repriced option continues at the end of the remaining

reporting period i.e. 31st March, 2019 and 31st March, 2020

= [Rs. 80 x 150 awards x 950 employees x (2 year / 3 years of service)] – Rs. 22,50,000

= Rs. 7,60,00,000 – Rs. 22,50,000 = Rs. 53,50,000

Journal Entries

31st March, 2018

Employee benefits expenses Dr. 22,50,000

To Share based payment liability 22,50,000

31st March, 2019

Employee benefits expenses Dr. 53,50,000

To Share based payment liability 53,50,000

(Fair value of the liability recognized)

31st March, 2020

Employee benefits expenses Dr. 35,60,000

To Share based payment liability 35,60,000

(Fair value of the liability recognized)

[(930 x 80 x 150) - 22,50,000 - 53,50,000]

Share based payment liability Dr. 1,11,60,000

To Bank 1,11,60,00

(Being liability for awards settled in cash)

(930 x 80 x 150)

nd

2 Alternative based on fair value at the grant date (ignoring the fact that the award has to be

settled in cash).

Calculation of expenses:

For the year ended 31st March 2018

= [Rs. 129 x 150 awards x 900 employees x (1 year /3 years of service)]

= Rs. 58,05,000

20. 28