Page 4 - 20. COMPILER QB - INDAS 102

P. 4

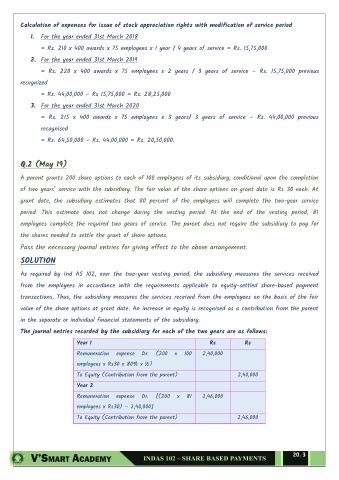

Calculation of expenses for issue of stock appreciation rights with modification of service period

1. For the year ended 31st March 2018

= Rs. 210 x 400 awards x 75 employees x 1 year / 4 years of service = Rs. 15,75,000

2. For the year ended 31st March 2019

= Rs. 220 x 400 awards x 75 employees x 2 years / 3 years of service – Rs. 15,75,000 previous

recognized

= Rs. 44,00,000 – Rs 15,75,000 = Rs. 28,25,000

3. For the year ended 31st March 2020

= Rs. 215 x 400 awards x 75 employees x 3 years/ 3 years of service – Rs. 44,00,000 previous

recognised

= Rs. 64,50,000 – Rs. 44,00,000 = Rs. 20,50,000.

Q.2 (May 19)

A parent grants 200 share options to each of 100 employees of its subsidiary, conditional upon the completion

of two years’ service with the subsidiary. The fair value of the share options on grant date is Rs 30 each. At

grant date, the subsidiary estimates that 80 percent of the employees will complete the two-year service

period. This estimate does not change during the vesting period. At the end of the vesting period, 81

employees complete the required two years of service. The parent does not require the subsidiary to pay for

the shares needed to settle the grant of share options.

Pass the necessary journal entries for giving effect to the above arrangement.

SOLUTION

As required by Ind AS 102, over the two-year vesting period, the subsidiary measures the services received

from the employees in accordance with the requirements applicable to equity-settled share-based payment

transactions. Thus, the subsidiary measures the services received from the employees on the basis of the fair

value of the share options at grant date. An increase in equity is recognised as a contribution from the parent

in the separate or individual financial statements of the subsidiary.

The journal entries recorded by the subsidiary for each of the two years are as follows:

Year 1 Rs Rs

Remuneration expense Dr. (200 x 100 2,40,000

employees x Rs30 x 80% x ½)

To Equity (Contribution from the parent) 2,40,000

Year 2

Remuneration expense Dr. [(200 x 81 2,46,000

employees x Rs30) – 2,40,000]

To Equity (Contribution from the parent) 2,46,000

20. 3