Page 18 - 23. COMPILER QB - IND AS 109_32

P. 18

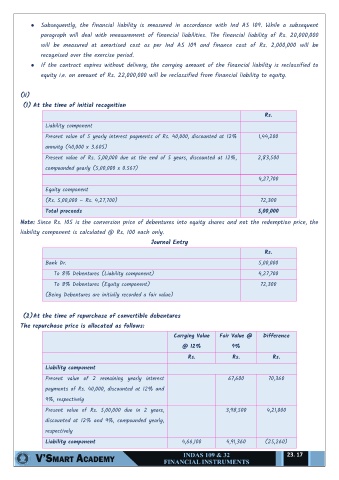

● Subsequently, the financial liability is measured in accordance with Ind AS 109. While a subsequent

paragraph will deal with measurement of financial liabilities. The financial liability of Rs. 20,000,000

will be measured at amortised cost as per Ind AS 109 and finance cost of Rs. 2,000,000 will be

recognised over the exercise period.

● If the contract expires without delivery, the carrying amount of the financial liability is reclassified to

equity i.e. an amount of Rs. 22,000,000 will be reclassified from financial liability to equity.

(ii)

(1) At the time of initial recognition

Rs.

Liability component

Present value of 5 yearly interest payments of Rs. 40,000, discounted at 12% 1,44,200

annuity (40,000 x 3.605)

Present value of Rs. 5,00,000 due at the end of 5 years, discounted at 12%, 2,83,500

compounded yearly (5,00,000 x 0.567)

4,27,700

Equity component

(Rs. 5,00,000 – Rs. 4,27,700) 72,300

Total proceeds 5,00,000

Note: Since Rs. 105 is the conversion price of debentures into equity shares and not the redemption price, the

liability component is calculated @ Rs. 100 each only.

Journal Entry

Rs.

Bank Dr. 5,00,000

To 8% Debentures (Liability component) 4,27,700

To 8% Debentures (Equity component) 72,300

(Being Debentures are initially recorded a fair value)

(2) At the time of repurchase of convertible debentures

The repurchase price is allocated as follows:

Carrying Value Fair Value @ Difference

@ 12% 9%

Rs. Rs. Rs.

Liability component

Present value of 2 remaining yearly interest 67,600 70,360

payments of Rs. 40,000, discounted at 12% and

9%, respectively

Present value of Rs. 5,00,000 due in 2 years, 3,98,500 4,21,000

discounted at 12% and 9%, compounded yearly,

respectively

Liability component 4,66,100 4,91,360 (25,260)

23. 17