Page 13 - 23. COMPILER QB - IND AS 109_32

P. 13

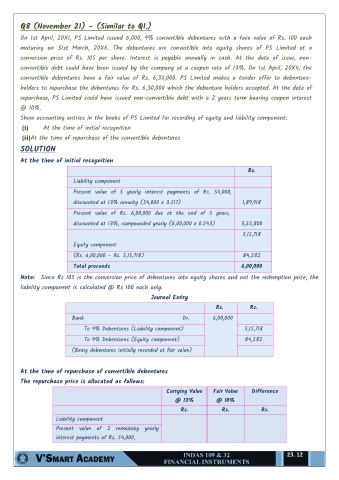

Q8 (November 21) – (Similar to Q1.)

On 1st April, 20X1, PS Limited issued 6,000, 9% convertible debentures with a face value of Rs. 100 each

maturing on 31st March, 20X6. The debentures are convertible into equity shares of PS Limited at a

conversion price of Rs. 105 per share. Interest is payable annually in cash. At the date of issue, non-

convertible debt could have been issued by the company at a coupon rate of 13%. On 1st April, 20X4, the

convertible debentures have a fair value of Rs. 6,30,000. PS Limited makes a tender offer to debenture-

holders to repurchase the debentures for Rs. 6,30,000 which the debenture holders accepted. At the date of

repurchase, PS Limited could have issued non-convertible debt with a 2 years term bearing coupon interest

@ 10%.

Show accounting entries in the books of PS Limited for recording of equity and liability component:

(i) At the time of initial recognition

(ii) At the time of repurchase of the convertible debentures

SOLUTION

At the time of initial recognition

Rs.

Liability component

Present value of 5 yearly interest payments of Rs. 54,000,

discounted at 13% annuity (54,000 x 3.517) 1,89,918

Present value of Rs. 6,00,000 due at the end of 5 years,

discounted at 13%, compounded yearly (6,00,000 x 0.543) 3,25,800

5,15,718

Equity component

(Rs. 6,00,000 – Rs. 5,15,718) 84,282

Total proceeds 6,00,000

Note: Since Rs 105 is the conversion price of debentures into equity shares and not the redemption price, the

liability component is calculated @ Rs 100 each only.

Journal Entry

Rs. Rs.

Bank Dr. 6,00,000

To 9% Debentures (Liability component) 5,15,718

To 9% Debentures (Equity component) 84,282

(Being debentures initially recorded at fair value)

At the time of repurchase of convertible debentures

The repurchase price is allocated as follows:

Carrying Value Fair Value Difference

@ 13% @ 10%

Rs. Rs. Rs.

Liability component

Present value of 2 remaining yearly

interest payments of Rs. 54,000,

23. 12