Page 16 - 23. COMPILER QB - IND AS 109_32

P. 16

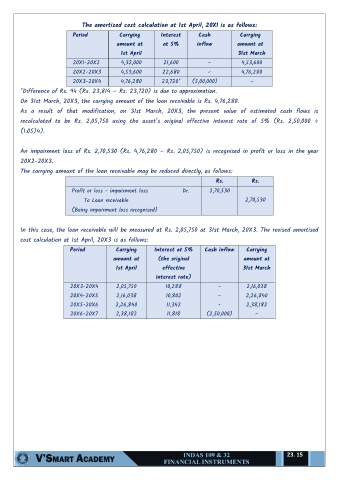

The amortised cost calculation at 1st April, 20X1 is as follows:

Period Carrying Interest Cash Carrying

amount at at 5% inflow amount at

1st April 31st March

20X1-20X2 4,32,000 21,600 – 4,53,600

20X2-20X3 4,53,600 22,680 – 4,76,280

20X3-20X4 4,76,280 23,720* (5,00,000) –

*Difference of Rs. 94 (Rs. 23,814 – Rs. 23,720) is due to approximation.

On 31st March, 20X3, the carrying amount of the loan receivable is Rs. 4,76,280.

As a result of that modification, on 31st March, 20X3, the present value of estimated cash flows is

recalculated to be Rs. 2,05,750 using the asset’s original effective interest rate of 5% (Rs. 2,50,000 ÷

(1.05)4).

An impairment loss of Rs. 2,70,530 (Rs. 4,76,280 – Rs. 2,05,750) is recognised in profit or loss in the year

20X2-20X3.

The carrying amount of the loan receivable may be reduced directly, as follows:

Rs. Rs.

Profit or loss - impairment loss Dr. 2,70,530

To Loan receivable 2,70,530

(Being impairment loss recognised)

In this case, the loan receivable will be measured at Rs. 2,05,750 at 31st March, 20X3. The revised amortised

cost calculation at 1st April, 20X3 is as follows:

Period Carrying Interest at 5% Cash inflow Carrying

amount at (the original amount at

1st April effective 31st March

interest rate)

20X3-20X4 2,05,750 10,288 – 2,16,038

20X4-20X5 2,16,038 10,802 – 2,26,840

20X5-20X6 2,26,840 11,342 – 2,38,182

20X6-20X7 2,38,182 11,818 (2,50,000) –

23. 15