Page 32 - 23. COMPILER QB - IND AS 109_32

P. 32

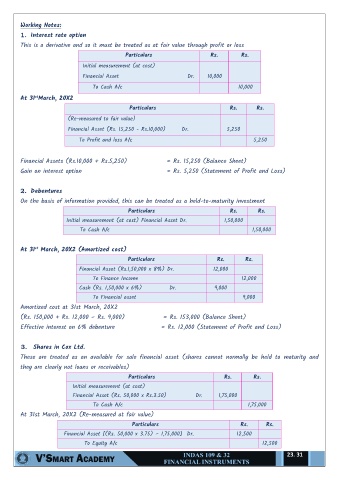

Working Notes:

1. Interest rate option

This is a derivative and so it must be treated as at fair value through profit or loss

Particulars Rs. Rs.

Initial measurement (at cost)

Financial Asset Dr. 10,000

To Cash A/c 10,000

st

At 31 March, 20X2

Particulars Rs. Rs.

(Re-measured to fair value)

Financial Asset (Rs. 15,250 - Rs.10,000) Dr. 5,250

To Profit and loss A/c 5,250

Financial Assets (Rs.10,000 + Rs.5,250) = Rs. 15,250 (Balance Sheet)

Gain on interest option = Rs. 5,250 (Statement of Profit and Loss)

2. Debentures

On the basis of information provided, this can be treated as a held-to-maturity investment

Particulars Rs. Rs.

Initial measurement (at cost) Financial Asset Dr. 1,50,000

To Cash A/c 1,50,000

st

At 31 March, 20X2 (Amortized cost)

Particulars Rs. Rs.

Financial Asset (Rs.1,50,000 x 8%) Dr. 12,000

To Finance Income 12,000

Cash (Rs. 1,50,000 x 6%) Dr. 9,000

To Financial asset 9,000

Amortized cost at 31st March, 20X2

(Rs. 150,000 + Rs. 12,000 – Rs. 9,000) = Rs. 153,000 (Balance Sheet)

Effective interest on 6% debenture = Rs. 12,000 (Statement of Profit and Loss)

3. Shares in Cox Ltd.

These are treated as an available for sale financial asset (shares cannot normally be held to maturity and

they are clearly not loans or receivables)

Particulars Rs. Rs.

Initial measurement (at cost)

Financial Asset (Rs. 50,000 x Rs.3.50) Dr. 1,75,000

To Cash A/c 1,75,000

At 31st March, 20X2 (Re-measured at fair value)

Particulars Rs. Rs.

Financial Asset [(Rs. 50,000 x 3.75) – 1,75,000] Dr. 12,500

To Equity A/c 12,500

23. 31