Page 69 - 23. COMPILER QB - IND AS 109_32

P. 69

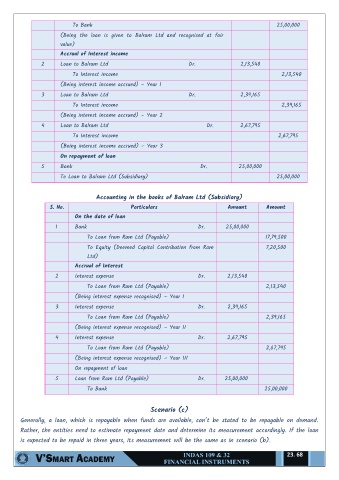

To Bank 25,00,000

(Being the loan is given to Balram Ltd and recognised at fair

value)

Accrual of Interest income

2 Loan to Balram Ltd Dr. 2,13,540

To Interest income 2,13,540

(Being interest income accrued) – Year 1

3 Loan to Balram Ltd Dr. 2,39,165

To Interest income 2,39,165

(Being interest income accrued) – Year 2

4 Loan to Balram Ltd Dr. 2,67,795

To Interest income 2,67,795

(Being interest income accrued) – Year 3

On repayment of loan

5 Bank Dr. 25,00,000

To Loan to Balram Ltd (Subsidiary) 25,00,000

Accounting in the books of Balram Ltd (Subsidiary)

S. No. Particulars Amount Amount

On the date of loan

1 Bank Dr. 25,00,000

To Loan from Ram Ltd (Payable) 17,79,500

To Equity (Deemed Capital Contribution from Ram 7,20,500

Ltd)

Accrual of Interest

2 Interest expense Dr. 2,13,540

To Loan from Ram Ltd (Payable) 2,13,540

(Being interest expense recognised) – Year I

3 Interest expense Dr. 2,39,165

To Loan from Ram Ltd (Payable) 2,39,165

(Being interest expense recognised) – Year II

4 Interest expense Dr. 2,67,795

To Loan from Ram Ltd (Payable) 2,67,795

(Being interest expense recognised) – Year III

On repayment of loan

5 Loan from Ram Ltd (Payable) Dr. 25,00,000

To Bank 25,00,000

Scenario (c)

Generally, a loan, which is repayable when funds are available, can’t be stated to be repayable on demand.

Rather, the entities need to estimate repayment date and determine its measurement accordingly. If the loan

is expected to be repaid in three years, its measurement will be the same as in scenario (b).

23. 68