Page 66 - 23. COMPILER QB - IND AS 109_32

P. 66

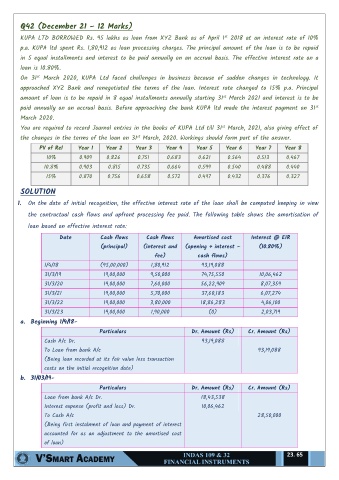

Q42 (December 21 – 12 Marks)

st

KUPA LTD BORROWED Rs. 95 lakhs as loan from XYZ Bank as of April 1 2018 at an interest rate of 10%

p.a. KUPA ltd spent Rs. 1,80,912 as loan processing charges. The principal amount of the loan is to be repaid

in 5 equal installments and interest to be paid annually on an accrual basis. The effective interest rate on a

loan is 10.80%.

st

On 31 March 2020, KUPA Ltd faced challenges in business because of sudden changes in technology. It

approached XYZ Bank and renegotiated the terms of the loan. Interest rate changed to 15% p.a. Principal

st

amount of loan is to be repaid in 8 equal installments annually starting 31 March 2021 and interest is to be

st

paid annually on an accrual basis. Before approaching the bank KUPA ltd made the interest payment on 31

March 2020.

st

You are required to record Journal entries in the books of KUPA Ltd till 31 March, 2021, also giving effect of

st

the changes in the terms of the loan on 31 March, 2020. Workings should form part of the answer.

PV of Rel Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

10% 0.909 0.826 0.751 0.683 0.621 0.564 0.513 0.467

10.8% 0.903 0.815 0.735 0.664 0.599 0.540 0.488 0.440

15% 0.870 0.756 0.658 0.572 0.497 0.432 0.376 0.327

SOLUTION

1. On the date of initial recognition, the effective interest rate of the loan shall be computed keeping in view

the contractual cash flows and upfront processing fee paid. The following table shows the amortisation of

loan based on effective interest rate:

Date Cash flows Cash flows Amortised cost Interest @ EIR

(principal) (interest and (opening + interest – (10.80%)

fee) cash flows)

1/4/18 (95,00,000) 1,80,912 93,19,088

31/3/19 19,00,000 9,50,000 74,75,550 10,06,462

31/3/20 19,00,000 7,60,000 56,22,909 8,07,359

31/3/21 19,00,000 5,70,000 37,60,183 6,07,274

31/3/22 19,00,000 3,80,000 18,86,283 4,06,100

31/3/23 19,00,000 1,90,000 (0) 2,03,719

a. Beginning 1/4/18-

Particulars Dr. Amount (Rs) Cr. Amount (Rs)

Cash A/c Dr. 93,19,088

To Loan from bank A/c 93,19,088

(Being loan recorded at its fair value less transaction

costs on the initial recognition date)

b. 31/03/19-

Particulars Dr. Amount (Rs) Cr. Amount (Rs)

Loan from bank A/c Dr. 18,43,538

Interest expense (profit and loss) Dr. 10,06,462

To Cash A/c 28,50,000

(Being first instalment of loan and payment of interest

accounted for as an adjustment to the amortised cost

of loan)

23. 65