Page 25 - 30. COMPILER QB - IND AS 101

P. 25

st

st

1 April 2019 was Rs. 95 lakhs. The carrying amount as of 1 April 2019 under the existing GAAP was

Rs. 42.75 lakhs.

ii) The company has recognized a provision for a proposed dividend of Rs. 5.7 lakhs and related dividend

st

distribution tax of Rs. 1.65 Lakhs during the year ended 31 March 2019. It was written back as on

the opening balance sheet date.

iii) The company had a non-integral foreign branch in accordance with AS 11 and had recognised a balance

of Rs. 2 lakhs as part of reserves. On first time adoption of Ind AS, the company intends to avail Ind

AS exemption of resetting the cumulative translation difference to zero.

iv) The company had made an investment in a subsidiary for Rs. 18.62 lakhs that carried a fair value of

Rs. 25.75 lakhs as at the transition date. The company intends to recognize the investment at its fair

value as at the date of transition.

v) The company has an Equity Share Capital of Rs. 760 lakhs and Redeemable Preference Share Capital

of Rs. 180 lakhs. The company identified that the preference shares were in the nature of financial

liabilities.

vi) The Reserves and Surplus as of 1 April 2019 before the transition to Ind AS was Rs. 910 lakhs

st

representing Rs. 380 lakhs of general reserve and Rs. 40 lakhs of Capital Reserve acquired out of

business combination and balance is surplus in the Retained Earnings.

st

What is the balance of total equity (Equity and other equity) as of 1 April 2019 after transitioning to Ind

AS? Show reconciliation between Total Equity as per AS (Accounting Standards) and as per Ind AS to be

presented in the opening balance sheet as on 1 April, 2019.

st

Ignore deferred tax impact.

Solution

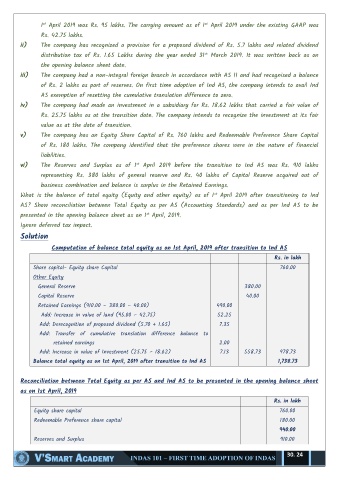

Computation of balance total equity as on 1st April, 2019 after transition to Ind AS

Rs. in lakh

Share capital- Equity share Capital 760.00

Other Equity

General Reserve 380.00

Capital Reserve 40.00

Retained Earnings (910.00 – 380.00 – 40.00) 490.00

Add: Increase in value of land (95.00 – 42.75) 52.25

Add: Derecognition of proposed dividend (5.70 + 1.65) 7.35

Add: Transfer of cumulative translation difference balance to

retained earnings 2.00

Add: Increase in value of Investment (25.75 – 18.62) 7.13 558.73 978.73

Balance total equity as on 1st April, 2019 after transition to Ind AS 1,738.73

Reconciliation between Total Equity as per AS and Ind AS to be presented in the opening balance sheet

as on 1st April, 2019

Rs. in lakh

Equity share capital 760.00

Redeemable Preference share capital 180.00

940.00

Reserves and Surplus 910.00

30. 24