Page 20 - 30. COMPILER QB - IND AS 101

P. 20

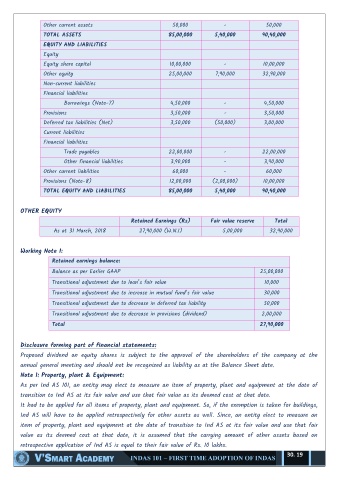

Other current assets 50,000 - 50,000

TOTAL ASSETS 85,00,000 5,40,000 90,40,000

EQUITY AND LIABILITIES

Equity

Equity share capital 10,00,000 - 10,00,000

Other equity 25,00,000 7,90,000 32,90,000

Non-current liabilities

Financial liabilities

Borrowings (Note-7) 4,50,000 - 4,50,000

Provisions 3,50,000 - 3,50,000

Deferred tax liabilities (Net) 3,50,000 (50,000) 3,00,000

Current liabilities

Financial liabilities

Trade payables 22,00,000 - 22,00,000

Other financial liabilities 3,90,000 - 3,90,000

Other current liabilities 60,000 - 60,000

Provisions (Note-8) 12,00,000 (2,00,000) 10,00,000

TOTAL EQUITY AND LIABILITIES 85,00,000 5,40,000 90,40,000

OTHER EQUITY

Retained Earnings (Rs) Fair value reserve Total

As at 31 March, 2018 27,90,000 (W.N.1) 5,00,000 32,90,000

Working Note 1:

Retained earnings balance:

Balance as per Earlier GAAP 25,00,000

Transitional adjustment due to loan’s fair value 10,000

Transitional adjustment due to increase in mutual fund’s fair value 30,000

Transitional adjustment due to decrease in deferred tax liability 50,000

Transitional adjustment due to decrease in provisions (dividend) 2,00,000

Total 27,90,000

Disclosure forming part of financial statements:

Proposed dividend on equity shares is subject to the approval of the shareholders of the company at the

annual general meeting and should not be recognized as liability as at the Balance Sheet date.

Note 1: Property, plant & Equipment:

As per Ind AS 101, an entity may elect to measure an item of property, plant and equipment at the date of

transition to Ind AS at its fair value and use that fair value as its deemed cost at that date.

It had to be applied for all items of property, plant and equipment. So, if the exemption is taken for buildings,

Ind AS will have to be applied retrospectively for other assets as well. Since, an entity elect to measure an

item of property, plant and equipment at the date of transition to Ind AS at its fair value and use that fair

value as its deemed cost at that date, it is assumed that the carrying amount of other assets based on

retrospective application of Ind AS is equal to their fair value of Rs. 10 lakhs.

30. 19