Page 14 - 33. FR RTP NOV. 22

P. 14

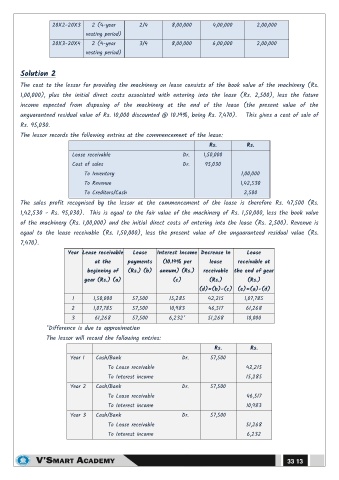

20X2-20X3 2 (4-year 2/4 8,00,000 4,00,000 2,00,000

vesting period)

20X3-20X4 2 (4-year 3/4 8,00,000 6,00,000 2,00,000

vesting period)

Solution 2

The cost to the lessor for providing the machinery on lease consists of the book value of the machinery (Rs.

1,00,000), plus the initial direct costs associated with entering into the lease (Rs. 2,500), less the future

income expected from disposing of the machinery at the end of the lease (the present value of the

unguaranteed residual value of Rs. 10,000 discounted @ 10.19%, being Rs. 7,470). This gives a cost of sale of

Rs. 95,030.

The lessor records the following entries at the commencement of the lease:

Rs. Rs.

Lease receivable Dr. 1,50,000

Cost of sales Dr. 95,030

To Inventory 1,00,000

To Revenue 1,42,530

To Creditors/Cash 2,500

The sales profit recognised by the lessor at the commencement of the lease is therefore Rs. 47,500 (Rs.

1,42,530 - Rs. 95,030). This is equal to the fair value of the machinery of Rs. 1,50,000, less the book value

of the machinery (Rs. 1,00,000) and the initial direct costs of entering into the lease (Rs. 2,500). Revenue is

equal to the lease receivable (Rs. 1,50,000), less the present value of the unguaranteed residual value (Rs.

7,470).

Year Lease receivable Lease Interest Income Decrease In Lease

at the payments (10.19% per lease receivable at

beginning of (Rs.) (b) annum) (Rs.) receivable the end of year

year (Rs.) (a) (c) (Rs.) (Rs.)

(d)=(b)-(c) (e)=(a)-(d)

1 1,50,000 57,500 15,285 42,215 1,07,785

2 1,07,785 57,500 10,983 46,517 61,268

3 61,268 57,500 6,232* 51,268 10,000

*Difference is due to approximation

The lessor will record the following entries:

Rs. Rs.

Year 1 Cash/Bank Dr. 57,500

To Lease receivable 42,215

To Interest income 15,285

Year 2 Cash/Bank Dr. 57,500

To Lease receivable 46,517

To Interest income 10,983

Year 3 Cash/Bank Dr. 57,500

To Lease receivable 51,268

To Interest income 6,232

33.13