Page 17 - 33. FR RTP NOV. 22

P. 17

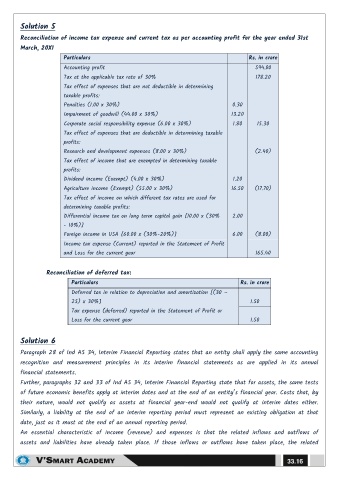

Solution 5

Reconciliation of income tax expense and current tax as per accounting profit for the year ended 31st

March, 20X1

Particulars Rs. in crore

Accounting profit 594.00

Tax at the applicable tax rate of 30% 178.20

Tax effect of expenses that are not deductible in determining

taxable profits:

Penalties (1.00 x 30%) 0.30

Impairment of goodwill (44.00 x 30%) 13.20

Corporate social responsibility expense (6.00 x 30%) 1.80 15.30

Tax effect of expenses that are deductible in determining taxable

profits:

Research and development expenses (8.00 x 30%) (2.40)

Tax effect of income that are exempted in determining taxable

profits:

Dividend income (Exempt) (4.00 x 30%) 1.20

Agriculture income (Exempt) (55.00 x 30%) 16.50 (17.70)

Tax effect of income on which different tax rates are used for

determining taxable profits:

Differential income tax on long term capital gain [10.00 x (30% 2.00

- 10%)]

Foreign income in USA [60.00 x (30%-20%)] 6.00 (8.00)

Income tax expense (Current) reported in the Statement of Profit

and Loss for the current year 165.40

Reconciliation of deferred tax:

Particulars Rs. in crore

Deferred tax in relation to depreciation and amortization [(30 –

25) x 30%] 1.50

Tax expense (deferred) reported in the Statement of Profit or

Loss for the current year 1.50

Solution 6

Paragraph 28 of Ind AS 34, Interim Financial Reporting states that an entity shall apply the same accounting

recognition and measurement principles in its interim financial statements as are applied in its annual

financial statements.

Further, paragraphs 32 and 33 of Ind AS 34, Interim Financial Reporting state that for assets, the same tests

of future economic benefits apply at interim dates and at the end of an entity‖s financial year. Costs that, by

their nature, would not qualify as assets at financial year-end would not qualify at interim dates either.

Similarly, a liability at the end of an interim reporting period must represent an existing obligation at that

date, just as it must at the end of an annual reporting period.

An essential characteristic of income (revenue) and expenses is that the related inflows and outflows of

assets and liabilities have already taken place. If those inflows or outflows have taken place, the related

33.16