Page 173 - CA Final PARAM Digital Book.

P. 173

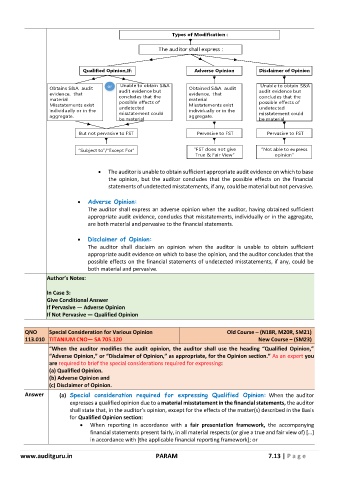

Types of Modification :

The auditor shall express :

Qualified Opinion,If: Adverse Opinion Disclaimer of Opinion

Obtains S&A audit or Unable to obtain S&A Obtained S&A audit Unable to obtain S&A

audit evidence but

audit evidence but

evidence, that concludes that the evidence, that concludes that the

material material

Misstatements exist possible effects of Misstatements exist possible effects of

undetected

individually or in the misstatement could individually or in the undetected

misstatement could

aggregate. be material aggregate. be material

But not pervasive to FST Pervasive to FST Pervasive to FST

Subject to Except For FST does not give Not able to express

True & Fair View opinion

• The auditor is unable to obtain sufficient appropriate audit evidence on which to base

the opinion, but the auditor concludes that the possible effects on the financial

statements of undetected misstatements, if any, could be material but not pervasive.

• Adverse Opinion:

The auditor shall express an adverse opinion when the auditor, having obtained sufficient

appropriate audit evidence, concludes that misstatements, individually or in the aggregate,

are both material and pervasive to the financial statements.

• Disclaimer of Opinion:

The auditor shall disclaim an opinion when the auditor is unable to obtain sufficient

appropriate audit evidence on which to base the opinion, and the auditor concludes that the

possible effects on the financial statements of undetected misstatements, if any, could be

both material and pervasive.

Author’s Notes:

In Case 3:

Give Conditional Answer

If Pervasive — Adverse Opinion

If Not Pervasive — Qualified Opinion

QNO Special Consideration for Various Opinion Old Course – (N18R, M20R, SM21)

113.010 TITANIUM CNO— SA 705.120 New Course – (SM23)

“When the auditor modifies the audit opinion, the auditor shall use the heading “Qualified Opinion,”

“Adverse Opinion,” or “Disclaimer of Opinion,” as appropriate, for the Opinion section.” As an expert you

are required to brief the special considerations required for expressing:

(a) Qualified Opinion.

(b) Adverse Opinion and

(c) Disclaimer of Opinion.

Answer (a) Special consideration required for expressing Qualified Opinion: When the auditor

expresses a qualified opinion due to a material misstatement in the financial statements, the auditor

shall state that, in the auditor’s opinion, except for the effects of the matter(s) described in the Basis

for Qualified Opinion section:

• When reporting in accordance with a fair presentation framework, the accompanying

financial statements present fairly, in all material respects (or give a true and fair view of) […]

in accordance with [the applicable financial reporting framework]; or

www.auditguru.in PARAM 7.13 | P a g e