Page 177 - CA Final PARAM Digital Book.

P. 177

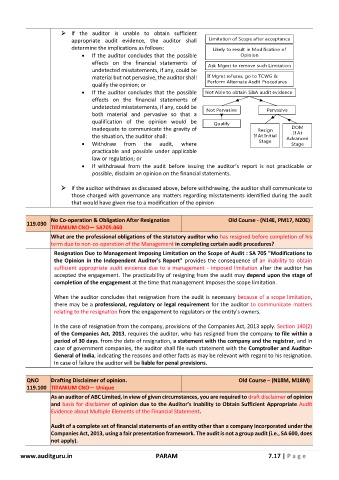

➢ If the auditor is unable to obtain sufficient

appropriate audit evidence, the auditor shall Limitation of Scope after acceptance

determine the implications as follows: Likely to result in Modification of

• If the auditor concludes that the possible Opinion

effects on the financial statements of Ask Mgmt to remove such Limitation

undetected misstatements, if any, could be

material but not pervasive, the auditor shall If Mgmt refuses, go to TCWG &

qualify the opinion; or Perform Alternate Audit Procedures

• If the auditor concludes that the possible Not Able to obtain S&A audit evidence

effects on the financial statements of

undetected misstatements, if any, could be Not Pervasive Pervasive

both material and pervasive so that a

qualification of the opinion would be Qualify

inadequate to communicate the gravity of Resign DOM

If At

the situation, the auditor shall: If At Initial Advanced

Stage

• Withdraw from the audit, where Stage

practicable and possible under applicable

law or regulation; or

• If withdrawal from the audit before issuing the auditor’s report is not practicable or

possible, disclaim an opinion on the financial statements.

➢ If the auditor withdraws as discussed above, before withdrawing, the auditor shall communicate to

those charged with governance any matters regarding misstatements identified during the audit

that would have given rise to a modification of the opinion

No Co-operation & Obligation After Resignation Old Course - (N14E, PM17, N20E)

119.030

TITANIUM CNO— SA705.060

What are the professional obligations of the statutory auditor who has resigned before completion of his

term due to non-co-operation of the Management in completing certain audit procedures?

Resignation Due to Management Imposing Limitation on the Scope of Audit : SA 705 "Modifications to

the Opinion in the Independent Auditor's Report" provides the consequence of an inability to obtain

sufficient appropriate audit evidence due to a management - imposed limitation after the auditor has

accepted the engagement. The practicability of resigning from the audit may depend upon the stage of

completion of the engagement at the time that management Imposes the scope limitation.

When the auditor concludes that resignation from the audit is necessary because of a scope limitation,

there may be a professional, regulatory or legal requirement for the auditor to communicate matters

relating to the resignation from the engagement to regulators or the entity's owners.

In the case of resignation from the company, provisions of the Companies Act, 2013 apply. Section 140(2)

of the Companies Act, 2013, requires the auditor, who has resigned from the company to file within a

period of 30 days. from the date of resignation, a statement with the company and the registrar, and in

case of government companies, the auditor shall file such statement with the Comptroller and Auditor-

General of India, indicating the reasons and other facts as may be relevant with regard to his resignation.

In case of failure the auditor will be liable for penal provisions.

QNO Drafting Disclaimer of opinion. Old Course – (N18M, M18M)

119.100 TITANIUM CNO— Unique

As an auditor of ABC Limited, in view of given circumstances, you are required to draft disclaimer of opinion

and basis for disclaimer of opinion due to the Auditor’s Inability to Obtain Sufficient Appropriate Audit

Evidence about Multiple Elements of the Financial Statement.

Audit of a complete set of financial statements of an entity other than a company incorporated under the

Companies Act, 2013, using a fair presentation framework. The audit is not a group audit (i.e., SA 600, does

not apply).

www.auditguru.in PARAM 7.17 | P a g e