Page 142 - CA Final Audit Titanium Full Book. (With Cover Pages)

P. 142

CA Ravi Taori

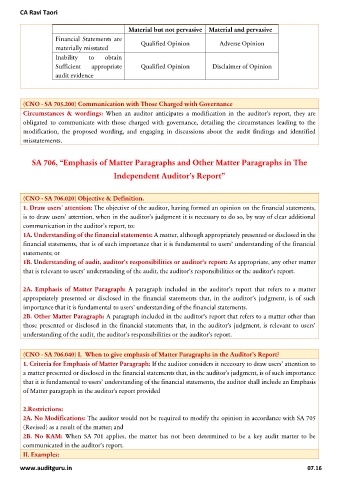

Material but not pervasive Material and pervasive

Financial Statements are

materially misstated Qualified Opinion Adverse Opinion

Inability to obtain

Sufficient appropriate Qualified Opinion Disclaimer of Opinion

audit evidence

(CNO - SA 705.200) Communication with Those Charged with Governance

Circumstances & wordings: When an auditor anticipates a modification in the auditor's report, they are

obligated to communicate with those charged with governance, detailing the circumstances leading to the

modification, the proposed wording, and engaging in discussions about the audit findings and identified

misstatements.

SA 706, “Emphasis of Matter Paragraphs and Other Matter Paragraphs in The

Independent Auditor’s Report”

(CNO - SA 706.020) Objective & Definition.

1. Draw users’ attention: The objective of the auditor, having formed an opinion on the financial statements,

is to draw users’ attention, when in the auditor’s judgment it is necessary to do so, by way of clear additional

communication in the auditor’s report, to:

1A. Understanding of the financial statements: A matter, although appropriately presented or disclosed in the

financial statements, that is of such importance that it is fundamental to users’ understanding of the financial

statements; or

1B. Understanding of audit, auditor’s responsibilities or auditor’s report: As appropriate, any other matter

that is relevant to users’ understanding of the audit, the auditor’s responsibilities or the auditor’s report.

2A. Emphasis of Matter Paragraph: A paragraph included in the auditor’s report that refers to a matter

appropriately presented or disclosed in the financial statements that, in the auditor’s judgment, is of such

importance that it is fundamental to users’ understanding of the financial statements.

2B. Other Matter Paragraph: A paragraph included in the auditor’s report that refers to a matter other than

those presented or disclosed in the financial statements that, in the auditor’s judgment, is relevant to users’

understanding of the audit, the auditor’s responsibilities or the auditor’s report.

(CNO - SA 706.040) I. When to give emphasis of Matter Paragraphs in the Auditor’s Report?

1. Criteria for Emphasis of Matter Paragraph: If the auditor considers it necessary to draw users’ attention to

a matter presented or disclosed in the financial statements that, in the auditor’s judgment, is of such importance

that it is fundamental to users’ understanding of the financial statements, the auditor shall include an Emphasis

of Matter paragraph in the auditor’s report provided

2.Restrictions:

2A. No Modifications: The auditor would not be required to modify the opinion in accordance with SA 705

(Revised) as a result of the matter; and

2B. No KAM: When SA 701 applies, the matter has not been determined to be a key audit matter to be

communicated in the auditor’s report.

II. Examples:

www.auditguru.in 07.16