Page 313 - CA Final Audit Titanium Full Book. (With Cover Pages)

P. 313

CA Ravi Taori

16 Internal Audit

Please note content related to SA 610 which deals with using work of internal auditor and taking direct

assistance of internal auditor is covered in Ch 3.

Case Study – Scale Limited

Independence Concern: CA. P. found it unusual that as a Chief Internal Auditor, he was to report to the CFO.

This could compromise his independence.

Reporting Structure: For maintaining independence, the Internal Auditor should report directly to the Audit

Committee, not to functions like Finance and Accounts.

Operational Roles: The offer letter mentioned roles in "system automation" and "process re-engineering,"

which are operational in nature. This could further compromise his independence.

Caveat: CA. P. communicated that he couldn't assume full accountability for these operational areas and

would only take on a limited role for a short duration.

Company's Agreement: The company acknowledged and agreed to CA. P.'s concerns.

Risk-Based Approach: After joining, CA. P. adopted a risk-based approach to identify key audit areas.

Error Prevention: CA. P. emphasized a system and process-focused approach to prevent errors, enhancing the

company's governance mechanisms.

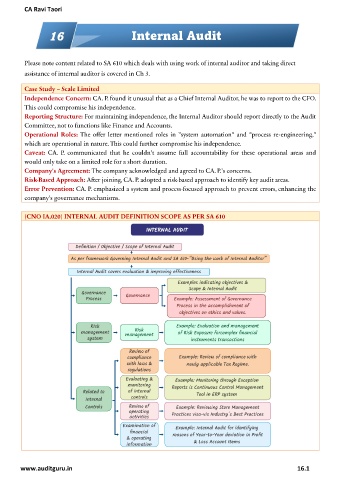

(CNO IA.020) INTERNAL AUDIT DEFINITION SCOPE AS PER SA 610

www.auditguru.in 16.1