Page 317 - CA Final Audit Titanium Full Book. (With Cover Pages)

P. 317

CA Ravi Taori

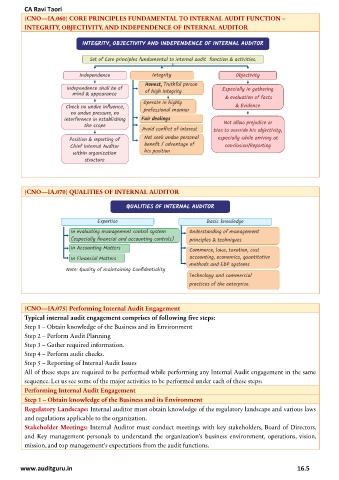

(CNO—IA.060) CORE PRINCIPLES FUNDAMENTAL TO INTERNAL AUDIT FUNCTION --

INTEGRITY, OBJECTIVITY, AND INDEPENDENCE OF INTERNAL AUDITOR

(CNO—IA.070) QUALITIES OF INTERNAL AUDITOR

(CNO—IA.075) Performing Internal Audit Engagement

Typical internal audit engagement comprises of following five steps:

Step 1 – Obtain knowledge of the Business and its Environment

Step 2 – Perform Audit Planning

Step 3 – Gather required information.

Step 4 – Perform audit checks.

Step 5 – Reporting of Internal Audit Issues

All of these steps are required to be performed while performing any Internal Audit engagement in the same

sequence. Let us see some of the major activities to be performed under each of these steps:

Performing Internal Audit Engagement

Step 1 – Obtain knowledge of the Business and its Environment

Regulatory Landscape: Internal auditor must obtain knowledge of the regulatory landscape and various laws

and regulations applicable to the organization.

Stakeholder Meetings: Internal Auditor must conduct meetings with key stakeholders, Board of Directors,

and Key management personals to understand the organization’s business environment, operations, vision,

mission, and top management’s expectations from the audit functions.

www.auditguru.in 16.5