Page 9 - Chap2 RCM

P. 9

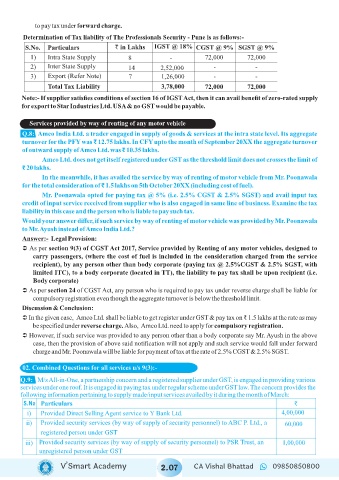

to pay tax under forward charge.

Determination of Tax liability of The Professionals Security - Pune is as follows:-

S.No. Particulars ` in Lakhs IGST @ 18% CGST @ 9% SGST @ 9%

1) Intra State Supply 8 - 72,000 72,000

2) Inter State Supply 14 2,52,000 - -

3) Export (Refer Note) 7 1,26,000 - -

Total Tax Liability 3,78,000 72,000 72,000

Note:- If supplier satisfies conditions of section 16 of IGST Act, then it can avail benefit of zero-rated supply

for export to Star Industries Ltd. USA & no GST would be payable.

Services provided by way of renting of any motor vehicle

Q.8: Amco India Ltd. a trader engaged in supply of goods & services at the intra state level. Its aggregate

turnover for the PFY was ₹ 12.75 lakhs. In CFY upto the month of September 20XX the aggregate turnover

of outward supply of Amco Ltd. was ₹ 10.35 lakhs.

Amco Ltd. does not get itself registered under GST as the threshold limit does not crosses the limit of

₹ 20 lakhs.

In the meanwhile, it has availed the service by way of renting of motor vehicle from Mr. Poonawala

for the total consideration of ₹ 1.5 lakhs on 5th October 20XX (including cost of fuel).

Mr. Poonawala opted for paying tax @ 5% (i.e. 2.5% CGST & 2.5% SGST) and avail input tax

credit of input service received from supplier who is also engaged in same line of business. Examine the tax

liability in this case and the person who is liable to pay such tax.

Would your answer differ, if such service by way of renting of motor vehicle was provided by Mr. Poonawala

to Mr. Ayush instead of Amco India Ltd.?

Answer:- Legal Provision:

Ü As per section 9(3) of CGST Act 2017, Service provided by Renting of any motor vehicles, designed to

carry passengers, (where the cost of fuel is included in the consideration charged from the service

recipient), by any person other than body corporate (paying tax @ 2.5%CGST & 2.5% SGST, with

limited ITC), to a body corporate (located in TT), the liability to pay tax shall be upon recipient (i.e.

Body corporate)

Ü As per section 24 of CGST Act, any person who is required to pay tax under reverse charge shall be liable for

compulsory registration even though the aggregate turnover is below the threshold limit.

Discussion & Conclusion:

Ü In the given case, Amco Ltd. shall be liable to get register under GST & pay tax on ₹ 1.5 lakhs at the rate as may

be specified under reverse charge. Also, Amco Ltd. need to apply for compulsory registration.

Ü However, if such service was provided to any person other than a body corporate say Mr. Ayush in the above

case, then the provision of above said notification will not apply and such service would fall under forward

charge and Mr. Poonawala will be liable for payment of tax at the rate of 2.5% CGST & 2.5% SGST.

02. Combined Questions for all services u/s 9(3):-

Q.9: M/s All-in-One, a partnership concern and a registered supplier under GST, is engaged in providing various

services under one roof. It is engaged in paying tax under regular scheme under GST law. The concern provides the

following information pertaining to supply made/input services availed by it during the month of March:

S.No Particulars `

i) Provided Direct Selling Agent service to Y Bank Ltd. 4,00,000

ii) Provided security services (by way of supply of security personnel) to ABC P. Ltd., a 60,000

registered person under GST

iii) Provided security services (by way of supply of security personnel) to PSR Trust, an 1,00,000

unregistered person under GST

V’Smart Academy 2.07 CA Vishal Bhattad 09850850800