Page 6 - Chapter 6_Value of Supply

P. 6

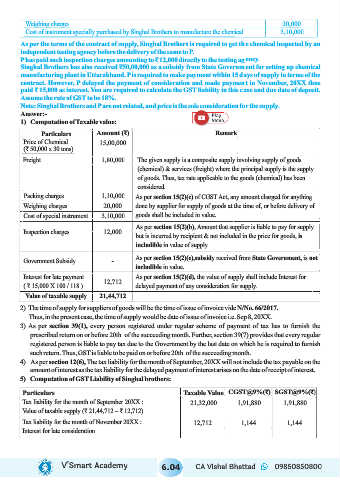

Weighing charges 20,000

Cost of instrument specially purchased by Singhal Brothers to manufacture the chemical 3,10,000

As per the terms of the contract of supply, Singhal Brothers is required to get the chemical inspected by an

independent testing agency before the delivery of the same to P.

P has paid such inspection charges amounting to ₹ 12,000 directly to the testing agency.

Singhal Brothers has also received ₹50,00,000 as a subsidy from State Government for setting up chemical

manufacturing plant in Uttarakhand. P is required to make payment within 15 days of supply in terms of the

contract. However, P delayed the payment of consideration and made payment in November, 20XX thus

paid ₹ 15,000 as interest. You are required to calculate the GST liability in this case and due date of deposit.

Assume the rate of GST to be 18%.

Note: Singhal Brothers and P are not related, and price is the sole consideration for the supply.

Answer:-

1) Computation of Taxable value:

Particulars Amount (₹) Remark

Price of Chemical 15,00,000

(₹ 50,000 x 30 tons)

Freight 1,80,000 The given supply is a composite supply involving supply of goods

(chemical) & services (freight) where the principal supply is the supply

of goods. Thus, tax rate applicable to the goods (chemical) has been

considered.

Packing charges 1,10,000 As per section 15(2)(c) of CGST Act, any amount charged for anything

Weighing charges 20,000 done by supplier for supply of goods at the time of, or before delivery of

Cost of special instrument 3,10,000 goods shall be included in value.

As per section 15(2)(b), Amount that supplier is liable to pay for supply

Inspection charges 12,000

but is incurred by recipient & not included in the price for goods, is

includible in value of supply.

As per section 15(2)(e),subsidy received from State Government, is not

Government Subsidy -

includible in value.

Interest for late payment As per section 15(2)(d), the value of supply shall include Interest for

12,712

( ₹ 15,000 X 100 / 118 ) delayed payment of any consideration for supply.

Value of taxable supply 21,44,712

2) The time of supply for suppliers of goods will be the time of issue of invoice vide N/No. 66/2017.

Thus, in the present case, the time of supply would be date of issue of invoice i.e. Sep 8, 20XX.

3) As per section 39(1), every person registered under regular scheme of payment of tax has to furnish the

prescribed return on or before 20th of the succeeding month. Further, section 39(7) provides that every regular

registered person is liable to pay tax due to the Government by the last date on which he is required to furnish

such return. Thus, GST is liable to be paid on or before 20th of the succeeding month.

4) As per section 12(6), The tax liability for the month of September, 20XX will not include the tax payable on the

amount of interest as the tax liability for the delayed payment of interest arises on the date of receipt of interest.

5) Computation of GST Liability of Singhal brothers:

Particulars Taxable Value CGST@9%(₹) SGST@9%(₹)

Tax liability for the month of September 20XX : 21,32,000 1,91,880 1,91,880

Value of taxable supply (₹ 21,44,712 – ₹ 12,712)

Tax liability for the month of November 20XX : 12,712 1,144 1,144

Interest for late consideration

V’Smart Academy 6.04 CA Vishal Bhattad 09850850800