Page 8 - Chapter 6_Value of Supply

P. 8

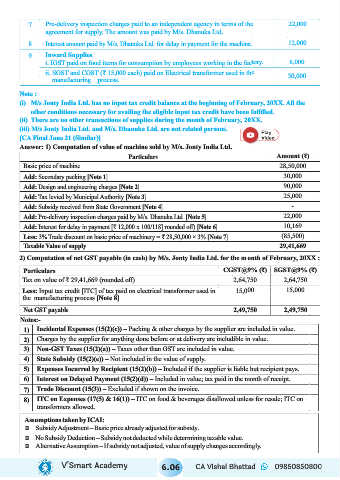

7 Pre-delivery inspection charges paid to an independent agency in terms of the 22,000

agreement for supply. The amount was paid by M/s. Dhanuka Ltd.

8 Interest amount paid by M/s. Dhanuka Ltd. for delay in payment for the machine. 12,000

9 Inward Supplies

i. IGST paid on food items for consumption by employees working in the factory. 8,000

ii. SGST and CGST (₹ 15,000 each) paid on Electrical transformer used in the

manufacturing process. 30,000

Note :

(i) M/s Jonty India Ltd. has no input tax credit balance at the beginning of February, 20XX. All the

other conditions necessary for availing the eligible input tax credit have been fulfilled.

(ii) There are no other transactions of supplies during the month of February, 20XX.

(iii) M/s Jonty India Ltd. and M/s. Dhanuka Ltd. are not related persons.

[CA Final June 21 (Similar)]

Answer: 1) Computation of value of machine sold by M/s. Jonty India Ltd.

Particulars Amount (₹)

Basic price of machine 28,50,000

Add: Secondary packing [Note 1] 30,000

Add: Design and engineering charges [Note 2] 90,000

Add: Tax levied by Municipal Authority [Note 3] 25,000

Add: Subsidy received from State Government [Note 4] -

Add: Pre-delivery inspection charges paid by M/s. Dhanuka Ltd. [Note 5] 22,000

Add: Interest for delay in payment [₹ 12,000 x 100/118] rounded off) [Note 6] 10,169

Less: 3% Trade discount on basic price of machinery = ₹ 28,50,000 × 3% [Note 7] (85,500)

Taxable Value of supply 29,41,669

2) Computation of net GST payable (in cash) by M/s. Jonty India Ltd. for the month of February, 20XX :

Particulars CGST@9% (₹) SGST@9% (₹)

Tax on value of ₹ 29,41,669 (rounded off) 2,64,750 2,64,750

Less: Input tax credit [ITC] of tax paid on electrical transformer used in 15,000 15,000

the manufacturing process [Note 8]

Net GST payable 2,49,750 2,49,750

Notes:-

1) Incidental Expenses (15(2)(c)) – Packing & other charges by the supplier are included in value.

2) Charges by the supplier for anything done before or at delivery are includible in value.

3) Non-GST Taxes (15(2)(a)) – Taxes other than GST are included in value.

4) State Subsidy (15(2)(e)) – Not included in the value of supply.

5) Expenses Incurred by Recipient (15(2)(b)) – Included if the supplier is liable but recipient pays.

6) Interest on Delayed Payment (15(2)(d)) – Included in value; tax paid in the month of receipt.

7) Trade Discount (15(3)) – Excluded if shown on the invoice.

8) ITC on Expenses (17(5) & 16(1)) – ITC on food & beverages disallowed unless for resale; ITC on

transformers allowed.

Assumptions taken by ICAI:

Ü Subsidy Adjustment – Basic price already adjusted for subsidy.

Ü No Subsidy Deduction – Subsidy not deducted while determining taxable value.

Ü Alternative Assumption – If subsidy not adjusted, value of supply changes accordingly.

V’Smart Academy 6.06 CA Vishal Bhattad 09850850800