Page 12 - Chap7 ITC

P. 12

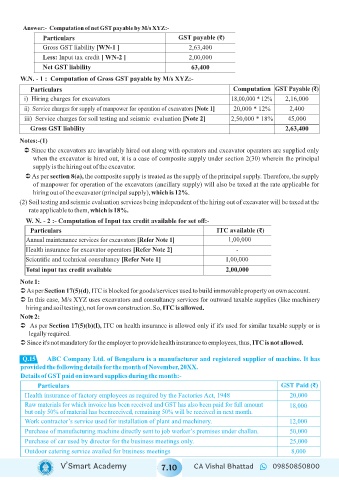

Answer:- Computation of net GST payable by M/s XYZ:-

Particulars GST payable ( )₹

Gross GST liability [WN-1 ] 2,63,400

Less: Input tax credit [ WN-2 ] 2,00,000

Net GST liability 63,400

W.N. - 1 : Computation of Gross GST payable by M/s XYZ:-

Particulars Computation GST Payable (₹)

i) Hiring charges for excavators 18,00,000 * 12% 2,16,000

ii) Service charges for supply of manpower for operation of excavators [Note 1] 20,000 * 12% 2,400

iii) Service charges for soil testing and seismic evaluation [Note 2] 2,50,000 * 18% 45,000

Gross GST liability 2,63,400

Notes:-(1)

Ü Since the excavators are invariably hired out along with operators and excavator operators are supplied only

when the excavator is hired out, it is a case of composite supply under section 2(30) wherein the principal

supply is the hiring out of the excavator.

Ü As per section 8(a), the composite supply is treated as the supply of the principal supply. Therefore, the supply

of manpower for operation of the excavators (ancillary supply) will also be taxed at the rate applicable for

hiring out of the excavator (principal supply), which is 12%.

(2) Soil testing and seismic evaluation services being independent of the hiring out of excavator will be taxed at the

rate applicable to them, which is 18%.

W. N. - 2 :- Computation of Input tax credit available for set off:-

Particulars ITC available (₹)

Annual maintenance services for excavators [Refer Note 1] 1,00,000

Health insurance for excavator operators [Refer Note 2] -

Scientific and technical consultancy [Refer Note 1] 1,00,000

Total input tax credit available 2,00,000

Note 1:

Ü As per Section 17(5)(d), ITC is blocked for goods/services used to build immovable property on own account.

Ü In this case, M/s XYZ uses excavators and consultancy services for outward taxable supplies (like machinery

hiring and soil testing), not for own construction. So, ITC is allowed.

NotŸe 2:

Ü As per Section 17(5)(b)(I), ITC on health insurance is allowed only if it's used for similar taxable supply or is

legally required.

Ü Since it's not mandatory for the employer to provide health insurance to employees, thus, ITC is not allowed.

ABC Company Ltd. of Bengaluru is a manufacturer and registered supplier of machine. It has

Q.15

provided the following details for the month of November, 20XX.

Details of GST paid on inward supplies during the month:-

Particulars GST Paid (₹)

Health insurance of factory employees as required by the Factories Act, 1948 20,000

Raw materials for which invoice has been received and GST has also been paid for full amount 18,000

but only 50% of material has beenreceived, remaining 50% will be received in next month.

Work contractor’s service used for installation of plant and machinery. 12,000

Purchase of manufacturing machine directly sent to job worker’s premises under challan. 50,000

Purchase of car used by director for the business meetings only. 25,000

Outdoor catering service availed for business meetings 8,000

V’Smart Academy 7.10 CA Vishal Bhattad 09850850800