Page 14 - Chap7 ITC

P. 14

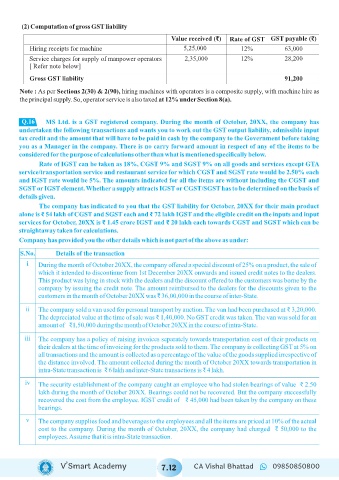

(2) Computation of gross GST liability

Value received ( )₹ Rate of GST GST payable )(₹

Hiring receipts for machine 5,25,000 12% 63,000

Service charges for supply of manpower operators 2,35,000 12% 28,200

[ Refer note below]

Gross GST liability 91,200

Note : As per Sections 2(30) & 2(90), hiring machines with operators is a composite supply, with machine hire as

the principal supply. So, operator service is also taxed at 12% under Section 8(a).

Q.16

MS Ltd. is a GST registered company. During the month of October, 20XX, the company has

undertaken the following transactions and wants you to work out the GST output liability, admissible input

tax credit and the amount that will have to be paid in cash by the company to the Government before taking

you as a Manager in the company. There is no carry forward amount in respect of any of the items to be

considered for the purpose of calculations other than what is mentioned specifically below.

Rate of IGST can be taken as 18%, CGST 9% and SGST 9% on all goods and services except GTA

service/transportation service and restaurant service for which CGST and SGST rate would be 2.50% each

and IGST rate would be 5%. The amounts indicated for all the items are without including the CGST and

SGST or IGST element. Whether a supply attracts IGST or CGST/SGST has to be determined on the basis of

details given.

The company has indicated to you that the GST liability for October, 20XX for their main product

alone is ₹ 54 lakh of CGST and SGST each and ₹ 72 lakh IGST and the eligible credit on the inputs and input

services for October, 20XX is ₹ 1.45 crore IGST and ₹ 20 lakh each towards CGST and SGST which can be

straightaway taken for calculations.

Company has provided you the other details which is not part of the above as under:

S.No. Details of the transaction

i During the month of October 20XX, the company offered a special discount of 25% on a product, the sale of

which it intended to discontinue from 1st December 20XX onwards and issued credit notes to the dealers.

This product was lying in stock with the dealers and the discount offered to the customers was borne by the

company by issuing the credit note. The amount reimbursed to the dealers for the discounts given to the

customers in the month of October 20XX was ₹ 36,00,000 in the course of inter-State.

ii The company sold a van used for personal transport by auction. The van had been purchased at ₹ 3,20,000.

The depreciated value at the time of sale was ₹ 1,40,000. No GST credit was taken. The van was sold for an

amount of ₹1,50,000 during the month of October 20XX in the course of intra-State.

iii The company has a policy of raising invoices separately towards transportation cost of their products on

their dealers at the time of invoicing for the products sold to them. The company is collecting GST at 5% on

all transactions and the amount is collected as a percentage of the value of the goods supplied irrespective of

the distance involved. The amount collected during the month of October 20XX towards transportation in

intra-State transaction is ₹ 6 lakh and inter-State transactions is ₹ 4 lakh.

iv The security establishment of the company caught an employee who had stolen bearings of value ₹ 2.50

lakh during the month of October 20XX. Bearings could not be recovered. But the company successfully

recovered the cost from the employee. IGST credit of ₹ 45,000 had been taken by the company on these

bearings.

v The company supplies food and beverages to the employees and all the items are priced at 10% of the actual

cost to the company. During the month of October, 20XX, the company had charged ₹ 50,000 to the

employees. Assume that it is intra-State transaction.

V’Smart Academy 7.12 CA Vishal Bhattad 09850850800